*) see also: InstaForex Trading Indicators for S&P 500 (SPX)

The outcome of the January Fed meeting and the nomination of Kevin Warsh create supportive conditions for further dollar strengthening, especially given expectations of tougher measures to contain inflation. However, the market remains cautious ahead of key economic releases, including the Non?Farm Payrolls report (on Friday) and the ISM PMI indices for the US manufacturing and services sectors, underscoring the need for careful assessment of the Fed's next steps, as well as the impact of ongoing geopolitical events and mostly unexpected actions by Trump and the White House — as noted in our today's review "USD in bullish correction."

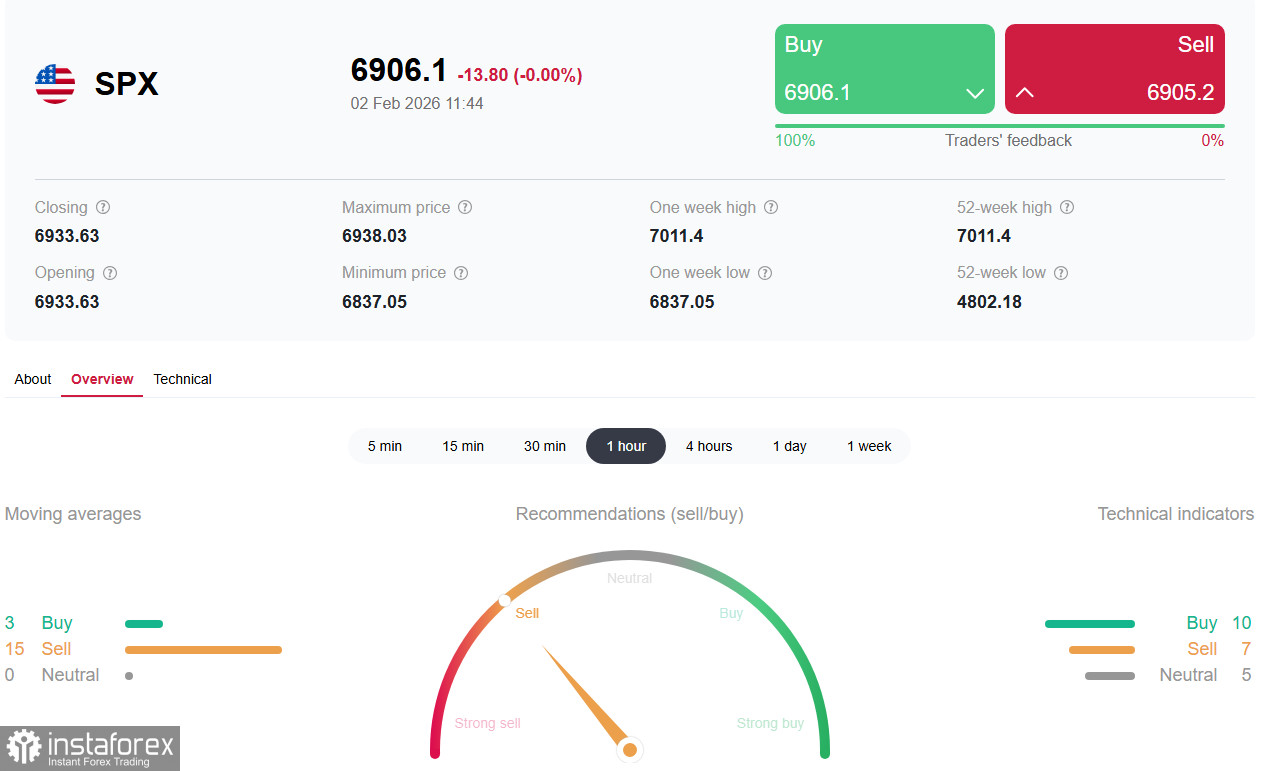

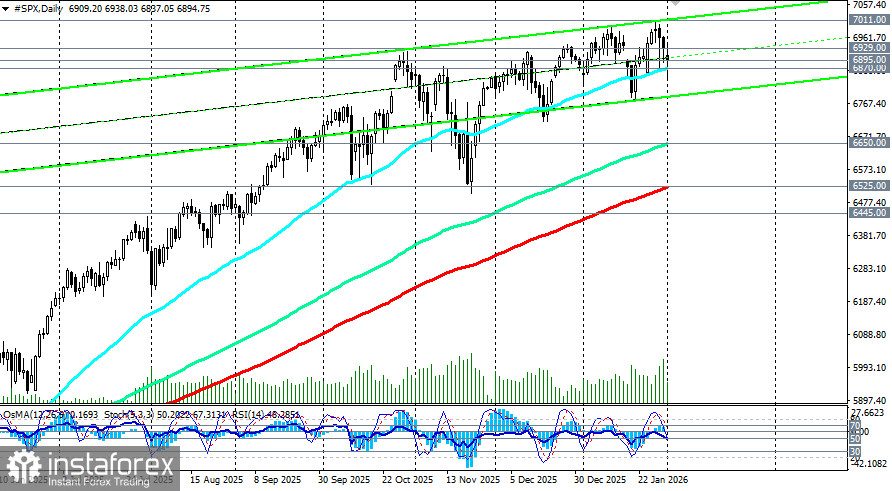

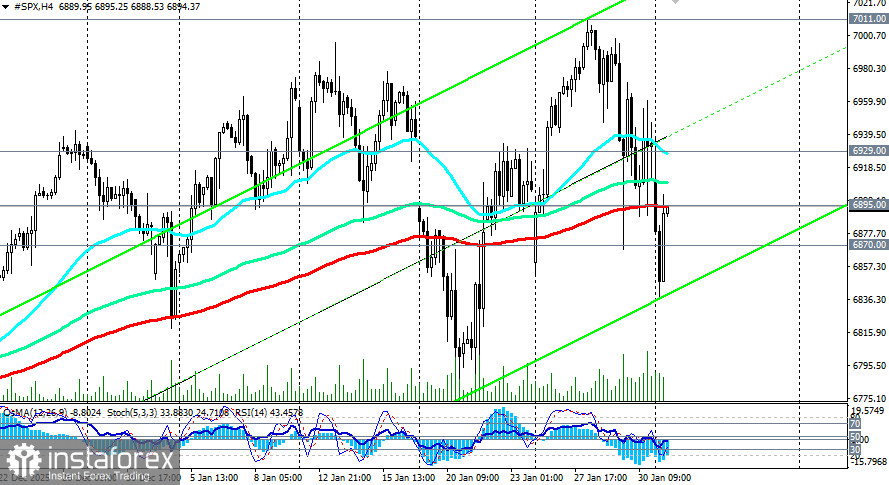

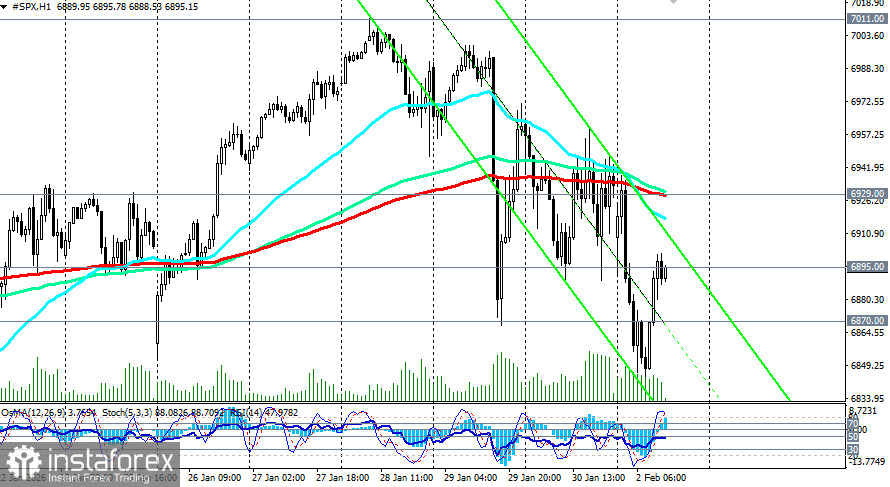

The leading barometer of the US economy — the S&P 500 index — is undergoing a local correction, trading before the opening level of Monday's US session around 6,895.00 (the 200?period moving average on the 4?hour chart). The week opened with a decline, and investor sentiment remains cautious.

The S&P 500 is traditionally viewed as a key gauge of the US equity market and the economy as a whole. It covers the largest US companies across sectors, from technology and finance to energy and industry, and reflects investors' expectations for corporate profits, monetary policy, and macroeconomic conditions.

Current dynamics are being shaped chiefly by three forces: staffing decisions at the Fed, the corporate earnings season, and rising macroeconomic uncertainty. The index remains sensitive to any shifts in rhetoric from regulators and policymakers.

Current dynamics: phase of local correction

The S&P 500 has entered a phase of a local correction, falling to an 8?day low near 6840.0 today.

Pressure on the market has intensified against the backdrop of several factors.

- First, investors reacted negatively to President Donald Trump's remarks about a likely successor to Jerome Powell as Fed chair. The nomination of Kevin Warsh, known for his preference for tighter monetary discipline and a stronger dollar, has raised near?term volatility in equity and debt markets. Such announcements increase uncertainty about future interest rate policy and the Fed's balance sheet path, which traditionally reduces risk appetite.

- Second, additional pressure came from corporate results in the energy sector. Revenue and profit downgrades at Exxon Mobil and Chevron amplified investor concerns about the sustainability of earnings amid geopolitical constraints and volatile commodity prices.

- Third, the broader backdrop is complicated by several macroeconomic and geopolitical factors:

- Macroeconomic factors: labor market and business activity. Key near?term market events include the Non?Farm Payrolls (NFP) release and ISM business activity indices for the US manufacturing and services sectors.

Expectations for a modest improvement in the manufacturing PMI to around 48 points indicate that the sector remains in contraction (values below 50), although the pace of decline is slowing. Economists note that manufacturing weakness contrasts with relative resilience in services, producing a mixed economic picture. Weaker PMI readings would increase concerns about economic slowing. Conversely, strong labor market data would support the dollar and strengthen the Fed's case for maintaining rates, which could cap equity upside. A weak jobs report would raise hopes for earlier easing but simultaneously stoke recession fears.

- A partial US government shutdown that began on Monday adds institutional risk.

- Ongoing tensions around Iran and the prospect of new trade sanctions.

- Bond market reaction: a drop in government yields (10?year Treasuries fell to 4.210% from 4.251% on Thursday at the time of writing) signals a flight to quality and rising demand for Treasuries, while also reflecting expectations of a potential economic slowdown.

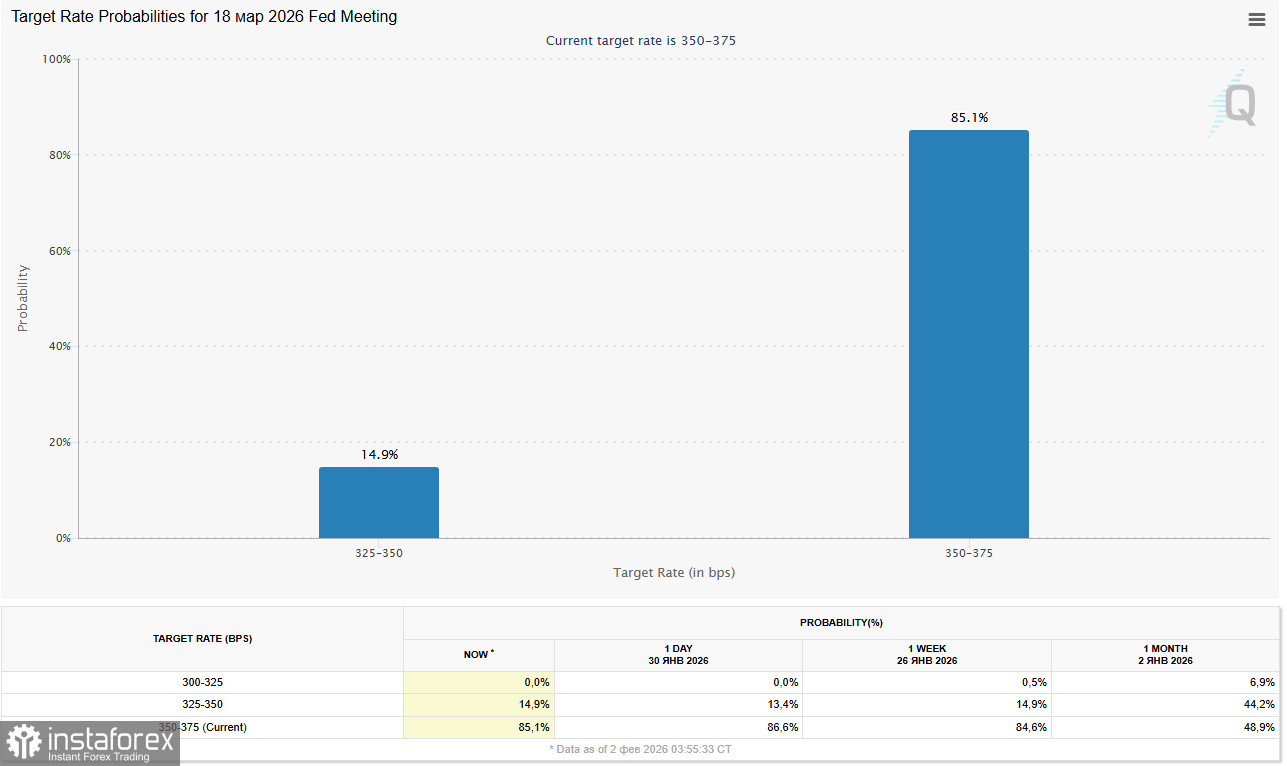

The fall in yields is accompanied by expectations that the Fed will keep policy rates on hold at least through upcoming meetings.

The CME FedWatch Tool shows the market is largely pricing a pause in rate changes until clearer signals on inflation and the labor market appear.

Technical analysis

Futures on the S&P 500 index (SPX on the trading platform) opened with a gap down and have settled in the "red" zone.

An important support area remains around 6,870.00 — close to the 50?day moving average. Holding this level is critical to prevent a deeper correction.

The nearest resistance is near 6,930.00 (200?period moving average on the 1?hour chart). A deepening correction scenario would be triggered by a break of the 6,870.00–6,800.00 support zone, targeting a move to 6,700.00–6,650.00 (144?period moving average on the daily chart).

Possible scenarios for the S&P 500:

- Consolidation scenario (most likely). The index will continue to trade sideways in the 6,800.00–6,950.00 range, with the market awaiting clarity from employment data and further commentary from Fed officials. Volatility will remain elevated.

- Recovery scenario may unfold if PMI and NFP data come in weaker than expected, prompting markets to price in the inevitability of earlier Fed easing despite Warsh's nomination and hawkish rhetoric. The upside target would be a return to the 69,50.00–7,000.00 zone.

- Continued correction scenario occurs if employment data are strong and the Trump nominee sends clear hawkish signals. That would confirm a "higher?for?longer" rates narrative and could push the index to test deeper support levels.

Conclusion

Rising trade tensions, the risk of expanded sanctions, and a partial US government shutdown are increasing capital outflows from risk assets. Historically, such periods of uncertainty tend to produce elevated volatility and sectoral capital reallocation — toward defensive sectors and companies with resilient cash flows — rather than a prolonged market collapse.

The current S&P 500 dynamics also reflect a phase of heightened uncertainty and market adaptation to shifting expectations on monetary policy and political risks. A local correction looks logical after the prior advance and does not necessarily signal the start of a long?term downtrend.

In the medium term, the fate of the US equity market will depend on the balance between inflation, the labor market, and Fed actions. For investors, this implies a need for a more measured approach, diversification, and heightened attention to macroeconomic signals that will shape the future path of the S&P 500.