Last week, reports in the Japanese press indicated that the Bank of Japan is not particularly prepared to raise rates at its April 28 meeting. In particular, it has been reported that three senior officials of the Bank of Japan do not seem too concerned about the sharp decline in market expectations for a rate hike in April and are not eager to change the situation, preferring instead to take a wait-and-see approach.

The consumer confidence index fell by 6.4 points in March compared to the previous month, to 33.3, marking the largest decline since an 8.9-point drop in April 2020, when authorities declared the first state of emergency in response to the COVID pandemic. It appears that the Bank of Japan is genuinely worried about the scenario in which it raises rates while the economy subsequently deteriorates significantly due to the energy crisis.

It seems that other factors, aside from inflation, are now playing a considerable role in the overall picture. The Bank of Japan has kept rates at minimal levels for too long, even as inflation rose to an uncomfortably high level, fearing a return to deflation that it has been unsuccessfully battling for decades. Numerous surveys indicate that business sentiment is rapidly deteriorating.

On Thursday evening, the March consumer price index report will be released. Inflation growth is expected to continue, but if the Bank of Japan signals its unwillingness to raise rates, there will be almost no factors supporting the yen. The Takaiichi government opposes raising rates, the Bank of Japan opposes it, and the threat of an economic slowdown is growing stronger. The yen literally has nothing to rely on except high inflation, and it is completely unclear how to find balance in conditions of total uncertainty.

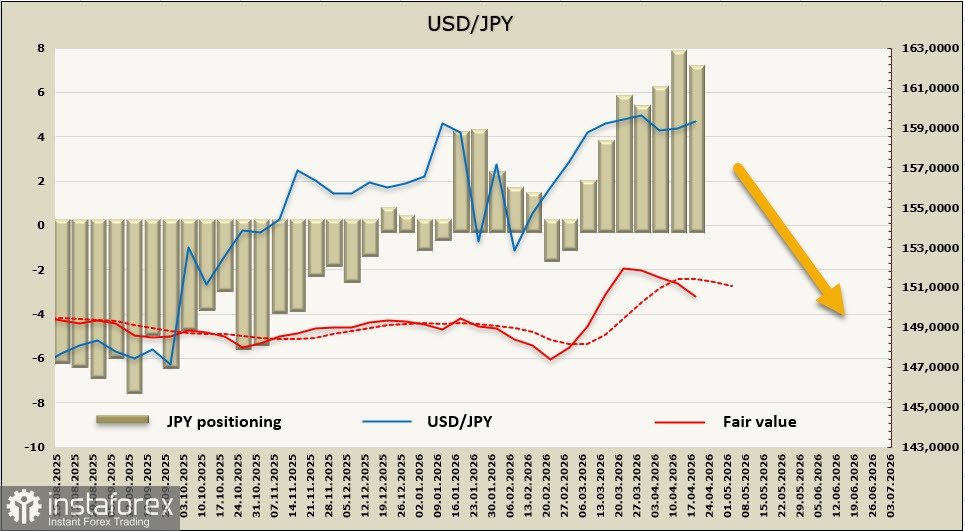

The net short position on the yen decreased by $0.79 billion over the reporting week to -$6.55 billion, with a bearish bias remaining high. At the same time, the calculated price is attempting to dip below the long-term average.

The yen is trading in a sideways range, and nothing has changed over the past week. All the same factors that have been in play previously continue to exert pressure, and therefore the forecast remains unchanged – the yen is objectively expected to weaken, especially as the likelihood of the Bank of Japan raising rates at the April meeting has decreased somewhat. We expect continued range trading, with growth to 162 and above remaining the priority scenario, but this must be confirmed by political events. A breakdown of the range downward to 156.00/50 is considered less likely.