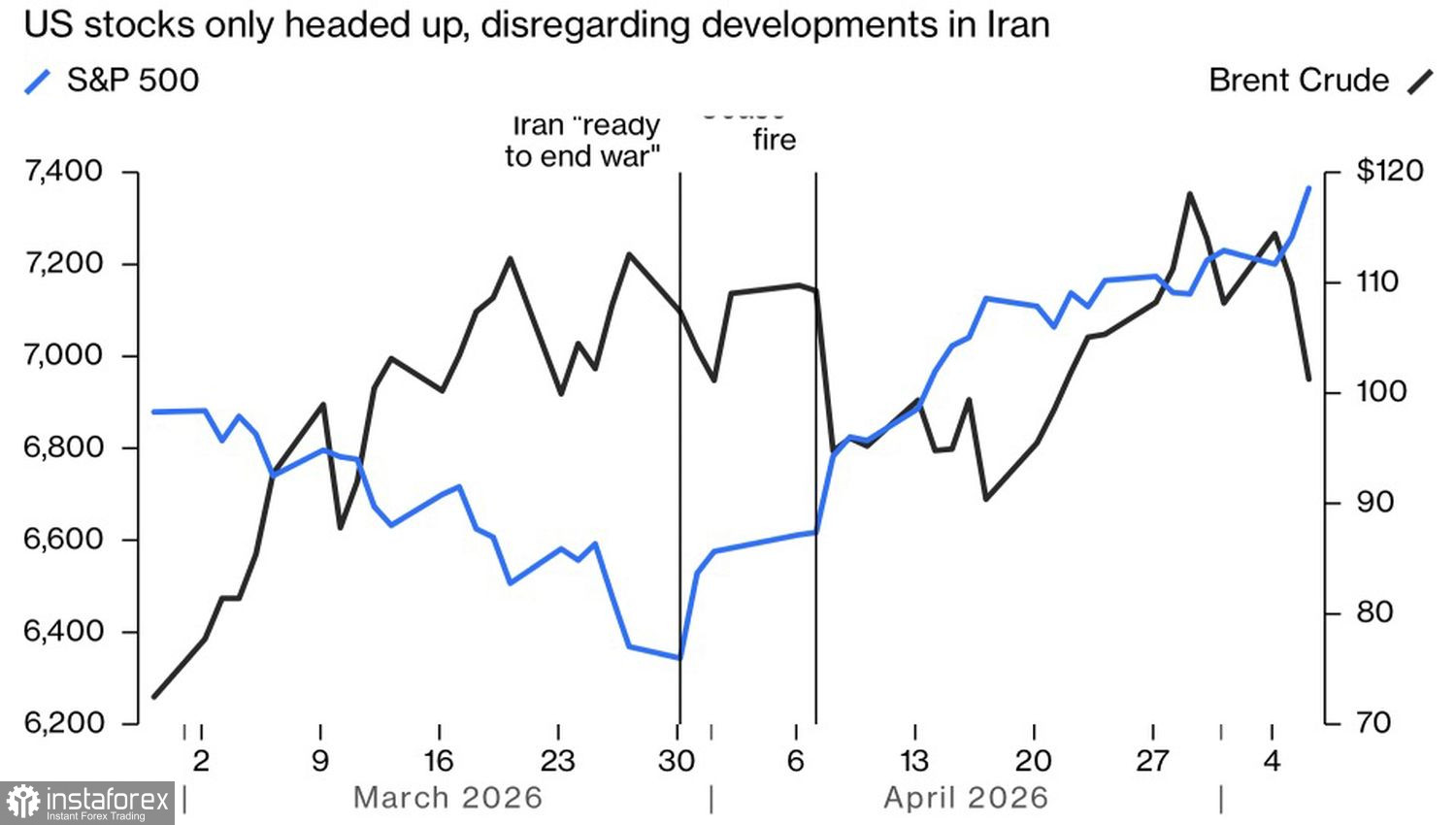

The US equity market continues to believe words over deeds. The S&P 500 posted a second consecutive record high after Donald Trump's comments that the Middle East war would end soon and that a deal would be struck before his meeting with Xi Jinping around the week of May 15. Investors seem unconcerned about the deal's details. Even the possibility that Iran retains its nuclear program is viewed as likely to lower oil prices and prevent inflation from re-accelerating if the geopolitical conflict becomes history.

For a long time, US equity indices were sensitive to oil dynamics, but at some point, the S&P 500 broke its correlation with Brent — it even turned negative for a time. It appears that markets have priced in the end of the Middle East confrontation as the base case. They were not deterred even by Tehran's breach of a ceasefire.

S&P 500 and oil dynamics

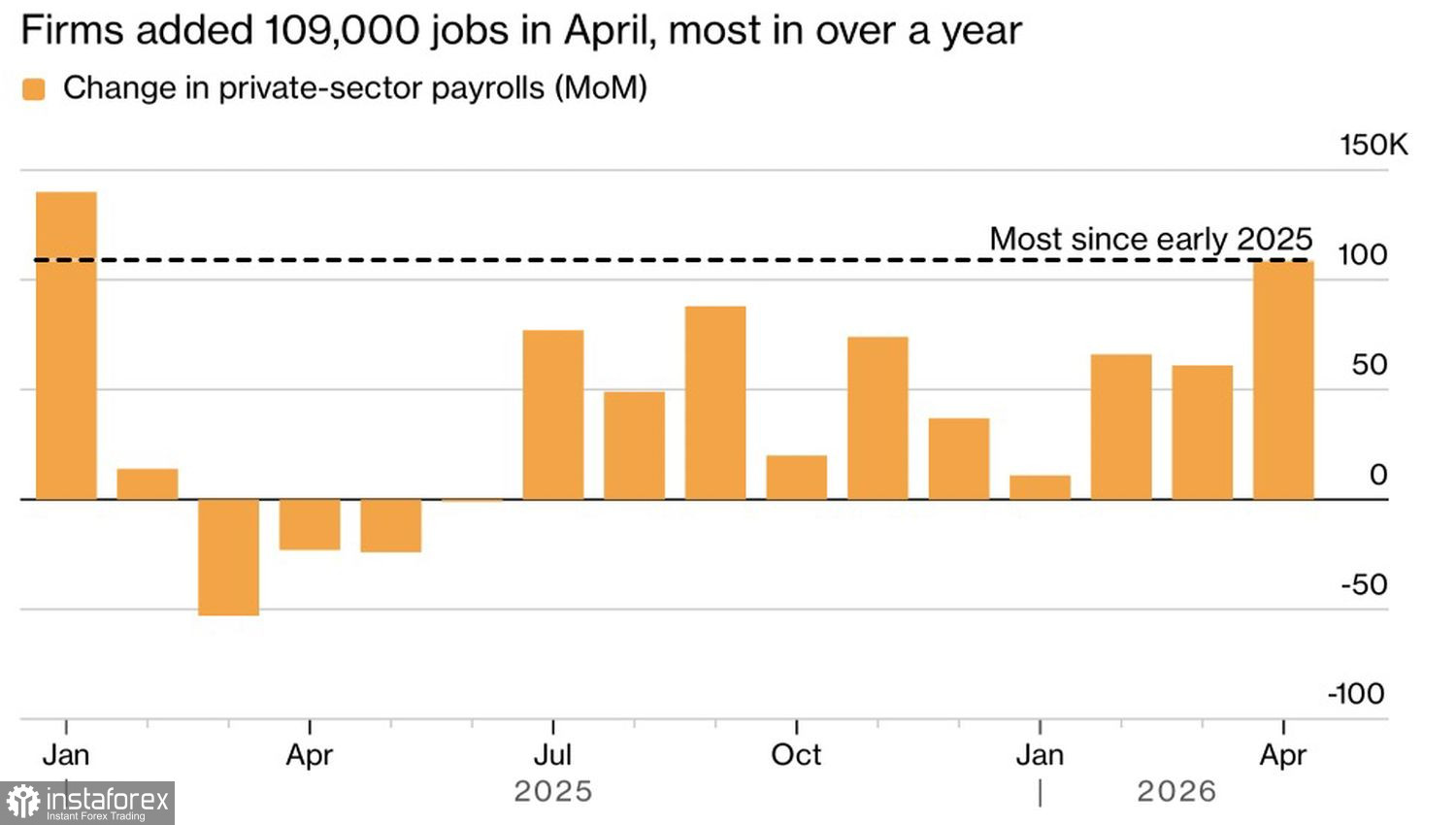

The S&P 500 has its own rally drivers: what were previously depressed fundamental valuations, impressive corporate earnings, tax incentives, and the underlying strength of the US economy. What more is needed for an upward move? Indeed, roughly 80% of S&P constituents that have reported have beaten earnings expectations, and ADP's fastest private sector job growth since January 2025 is further evidence that the US economy remains on a solid footing.

It will be interesting to observe the S&P 500's reaction to the BLS April US jobs report. Will weak payrolls be used as a rationale to buy equities? In this scenario, the odds of looser Fed policy would rise, which, in theory, should support the broad index.

US private sector employment dynamics

Conversely, the S&P 500 has plenty of trump cards to ignore monetary policy — strong nonfarm payroll numbers could lift the index even further.

Additional support for US equities could come from problems among their competitors. Currency interventions in Japan aimed at rescuing the sinking yen signal government use of non-market measures. That raises political risk and encourages capital flight.

Europe faces different challenges. Whether the EU has delayed ratifying a deal with the US, or Friedrich Merz's offhand remark that "Iran is embarrassing the US on a global stage," the result is heightened uncertainty. Meanwhile, Donald Trump's threat to raise tariffs on American cars from 15% to 25% is weighing on the EuroStoxx 600.

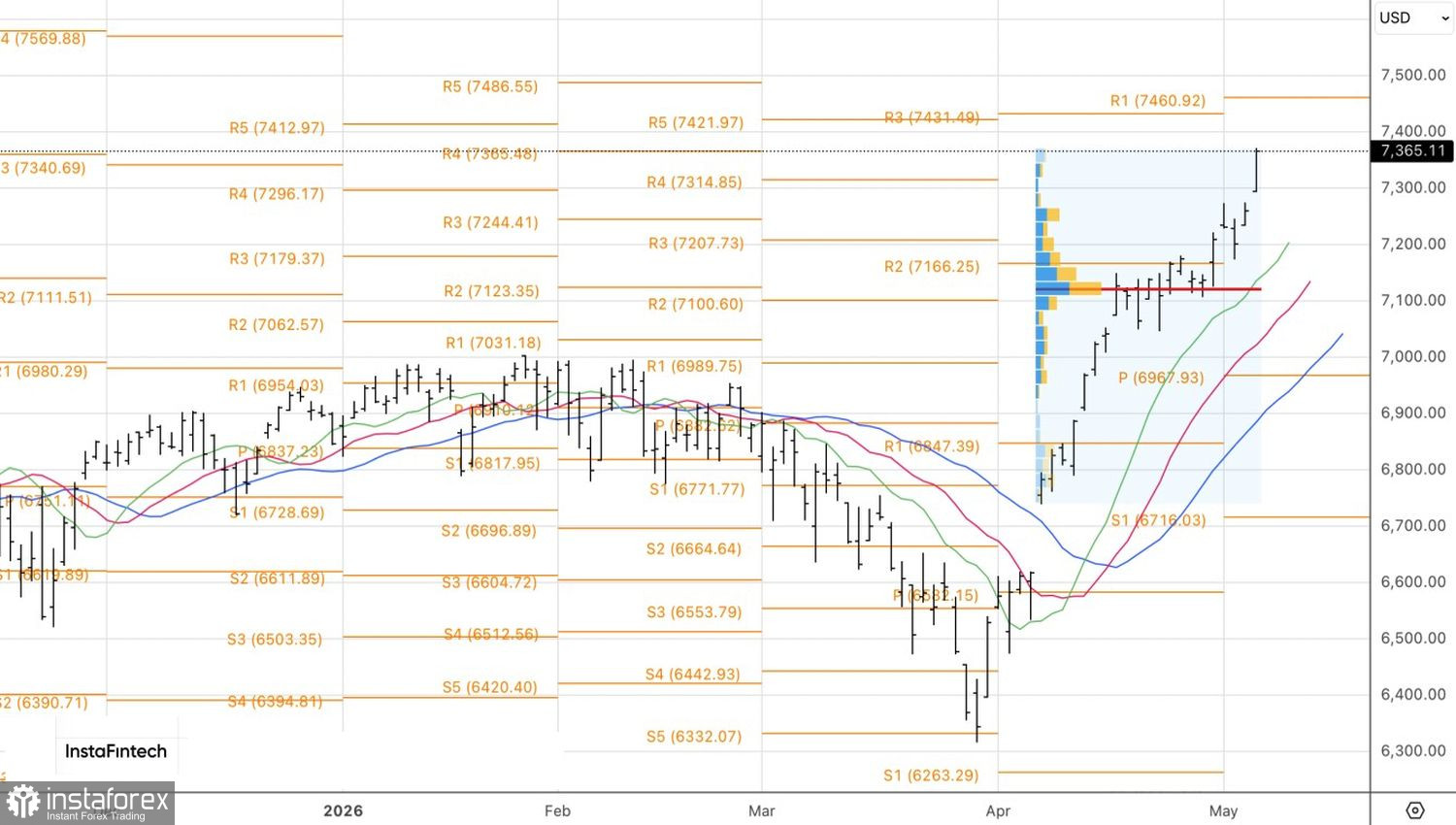

Technically, the daily S&P 500 chart shows acceleration of the uptrend, visible in the widening gap between prices and dynamic support levels such as exponential moving averages. Long positions targeting the previously identified levels of 7,429 and 7,500 remain valid.