The US dollar index enters the US trading session on Wednesday under modest pressure ahead of today's ISM Services PMI (14:00 GMT) and the ADP report (12:15 GMT), but generally holding the positions established earlier this week. Renewed escalation in the Strait of Hormuz (including retaliatory strikes on US bases in Kuwait and Bahrain) has again restored demand for the greenback as the principal safe-haven currency. A further supporting factor for the dollar has been hawkish labor market data (JOLTS), which reduce the likelihood of an imminent Fed easing.

Fundamental background: triple hawkish factor

Hopes of a diplomatic breakthrough that briefly weakened the dollar early this week were fully offset by a new wave of military escalation in the Persian Gulf.

Key developments in the past 24 hours

- US strikes on Iran. CENTCOM confirmed "self-defense strikes" against Iran's Qeshm Island in the Strait of Hormuz.

- Iran's response. The Islamic Revolutionary Guard Corps attacked US military facilities in Kuwait and Bahrain. Although air-defense systems intercepted the majority of rockets and drones, the attacks themselves represent an escalation.

- Crisis in Lebanon. Fighting between Israel and Hezbollah intensified, widening the zone of conflict.

This dynamic of reciprocal accusations and strikes, together with the absence of a diplomatic breakthrough, returned the geopolitical premium to prices almost instantly. The dollar index responded with gains as investors again sought refuge in the US currency.

Alongside geopolitics, a repricing of Fed policy expectations on the back of strong labor market data has been a driver of dollar strength.

JOLTS data for April (Tuesday):

- Job openings jumped to 7.618 million (consensus 6.88 million), the highest level since May 2024.

- The openings rate rose from 4.2% to 4.6%. Fed governor and FOMC member Christopher Waller previously described the 4.6% level as critical for forecasting turning points in unemployment acceleration.

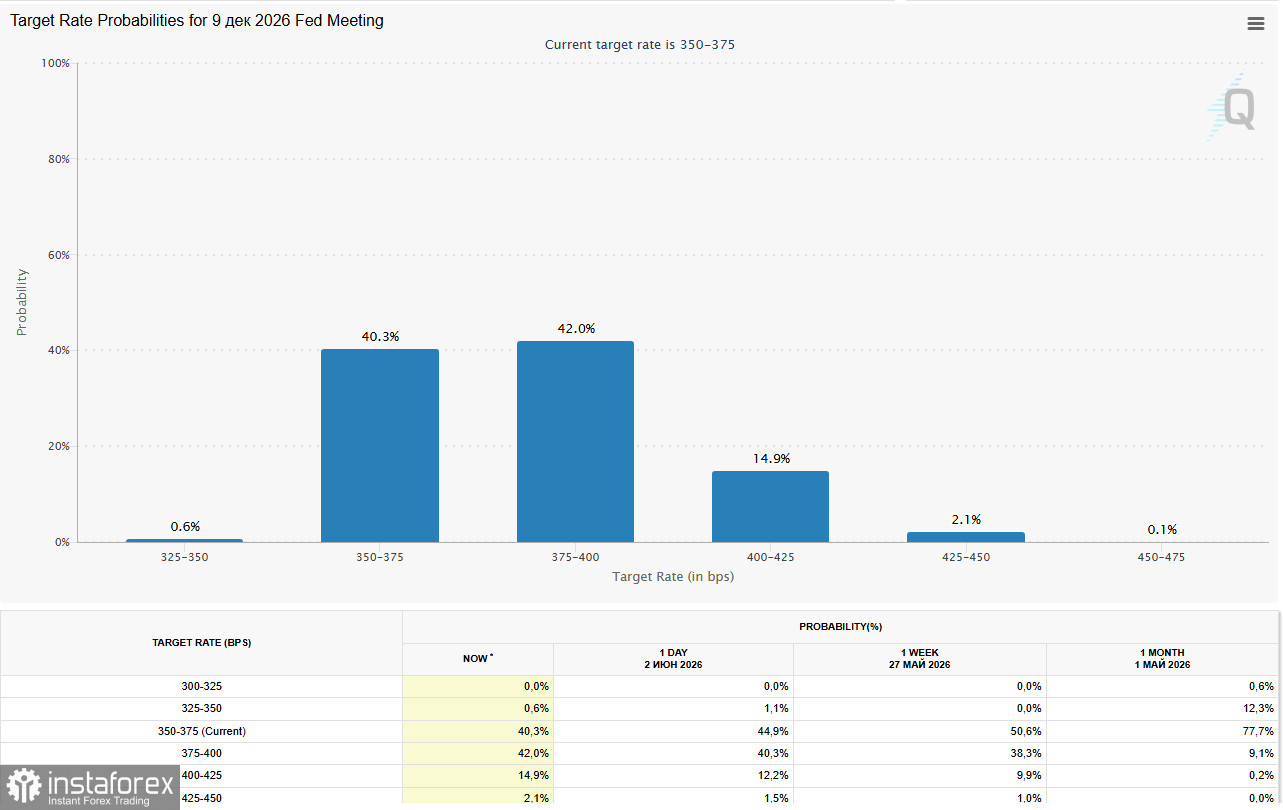

Markets reacted immediately. According to the CME FedWatch tool, the probability of a Fed rate hike in December has surpassed 50%.

Two-year Treasury yields settled above 4.05% and 10-year yields above 4.46%.

In addition to the data, Fed officials continued to send hawkish signals. Cleveland Fed President Loretta Mester said the central bank is firmly committed to returning inflation to 2% and "may need to act soon" if inflationary trends do not cool.

| Factor | Influence on USDX | Comments |

| Escalation of the conflict (Iran) | Support | Demand for the dollar as a safe haven. |

| JOLTS data (7.618 million) | Support | Overheated labor market, stronger hawkish expectations |

| Probability of a Fed rate increase (over 50%) — | Support | Market expectations shifted toward tightening. |

| Fed officials' comments | Support | Hawkish rhetoric, signals of possible action. |

| Pause in US-Iran talks | Support | Increased uncertainty and demand for the dollar. |

Key events today:

- 12:15 GMT — ADP employment change (May). Forecast: +120k (previous +109k). Expected impact: Strong figures will strengthen the dollar.

- 14:00 GMT — ISM Services PMI (May). Forecast: 53.8 (previous 53.6). Expected impact: Above-forecast reading will support the dollar.

- 14:00 GMT — ISM Services Employment Index. Forecast: improvement. Expected impact: Important labor market leading indicator.

- 14:00 GMT — ISM Services Prices Paid. Forecast: rise to 72.3. Expected impact: A rise would heighten inflation concerns.

- 18:00 GMT — Fed Beige Book release. Expected impact: Information on the state of the economy.

The main trigger of the week remains Friday's US nonfarm payrolls (May). The forecast is 85–95k; stronger figures would bolster the dollar.

Brief technical analysis

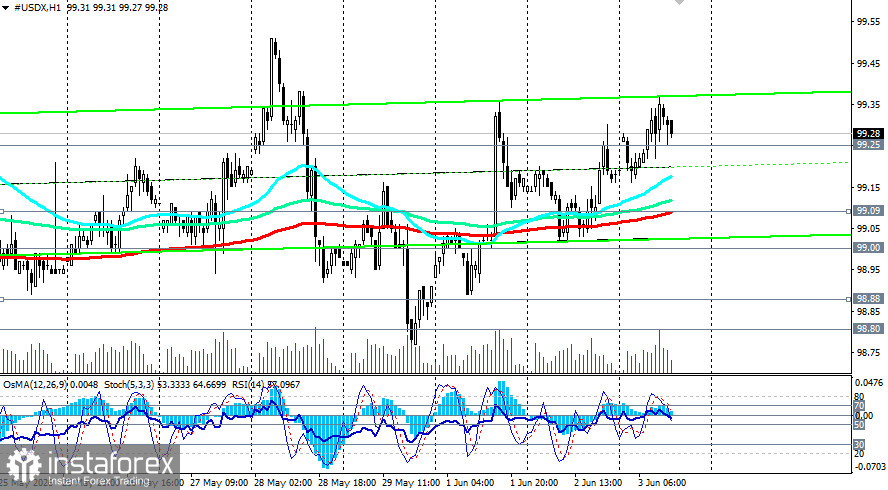

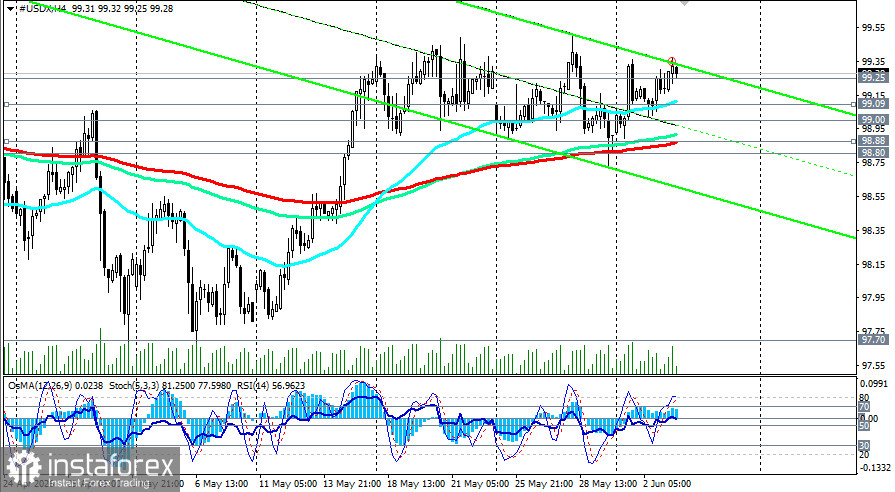

Technically, the USDX is consolidating above several important support levels: 99.09 (200-hour EMA on the 1-hour chart), 99.00 (round level and 200-day EMA on the daily chart), 98.88 (200-hour EMA on the 4-hour chart). The index is encountering strong resistance at 99.25 (50-week EMA), reflecting mixed fundamental signals.

Key technical signals

- The 200-day EMA sits at 99.00 and acts as a key dynamic support. The index successfully bounced from it this week.

- The RSI (14) is around 57–60, indicating positive but not overbought momentum.

Most economists conclude that renewed US-Iran tensions have supported the dollar, and that a restrictive Fed stance is viewed as further support for additional dollar strength.

They also expect the dollar index to continue consolidating, but strong labor data and geopolitical risks could push the dollar to break above 99.50.

The most likely near-term scenario is continued consolidation in the 98.70–99.50 range while markets wait for NFP and the weekend's geopolitical developments.

Conclusion

The USDX sits in a comfortable support zone supported by three factors:

- Geopolitical escalation in the Middle East restored demand for the dollar as a safe haven.

- Shockingly strong JOLTS data (7.618 million job openings) reduced expectations of Fed easing and increased the probability of a hike.

- Hawkish Fed commentary added to bullish conviction.

The key zone 99.00–99.50 will be the arena of a decisive battle in the coming days. Holding above 99.00 and a break of 99.50 would open the way to 100.00.

The US macro backdrop, which supports a tighter Fed stance, could contribute to further dollar appreciation, economists say, but they warn that the Fed leadership transition and geopolitical risks keep the dollar rangebound.

Investors should watch today's ISM Services PMI and the Beige Book, and Friday's NFP — these events will determine whether the dollar can hold above 99.50 and head to 100.00 or whether a correction will occur.

The USDX has found itself in a comfortable support zone formed by three factors. The key zone 99.00–99.50 will be the arena of a decisive battle in the coming days. Holding above 99.00 and a break of 99.50 would open the way to 100.00.

See also our today's reviews: