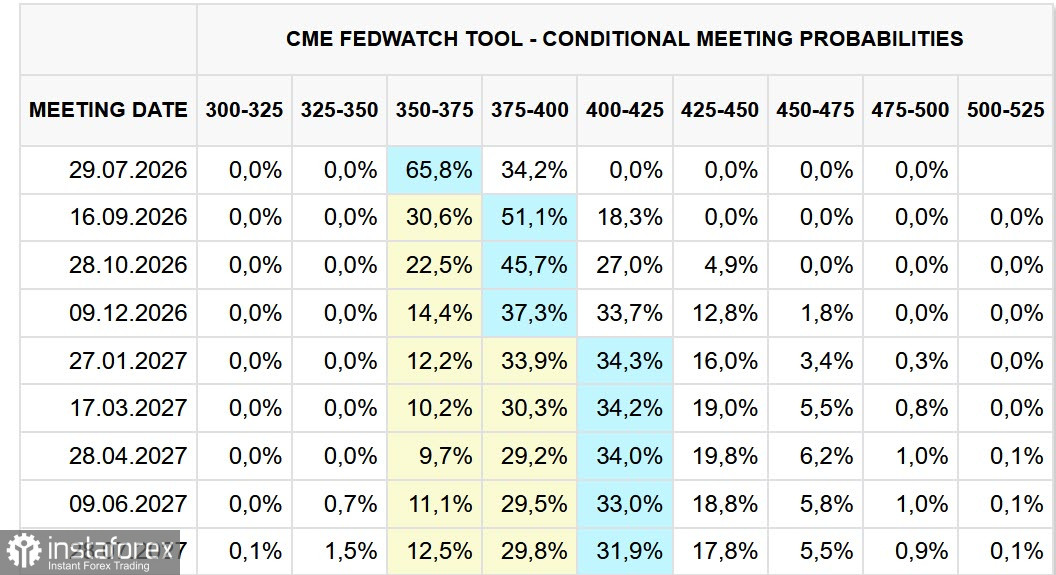

Global markets continue to react to the U.S. Federal Reserve's "hawkish" pivot, which has led to a significant strengthening of the dollar. If previously futures had suggested the first rate hike only in December, the market now anticipates it in September. Moreover, the likelihood of the Fed raising rates at its upcoming June meeting is increasing by the day. The trend towards easing policy has been unanimously canceled.

Additionally, several experts are calling for two rate hikes this year and another at the beginning of next year, ultimately bringing the rate to the 4.25%-4.50% range.

The U.S. economy appears strong, and it's worth noting that inflation began to rise even before the war in Iran, while core inflation has increased independently of it. Therefore, the peace agreement does not alleviate this pressure; investments are actively growing, as the Fed specifically noted in its accompanying statement. It appears that the focus is on a robust economy, and as long as economic momentum allows, the battle against inflation intensifies.

European Central Bank President Christine Lagarde stated on Monday that the ECB's rate hike was justified in all scenarios, but the current shock does not yet warrant decisive measures. Recent events remain within forecasts, and the ECB will continue to align its actions with incoming data. This stance is significantly weaker than the Fed's. Lagarde also noted that the conflict in the Middle East is putting pressure on economic activity, and incoming data indicate a slowdown in growth rates, particularly in the services sector. Lagarde expects that domestic demand will be weaker than projected in March.

The published PMI indices for the Eurozone today confirm Lagarde's statements: the composite index for June remained in contraction territory at 49.5 points. Following Lagarde's comments, the market reduced expectations of another ECB rate hike in the coming months, putting additional pressure on the euro.

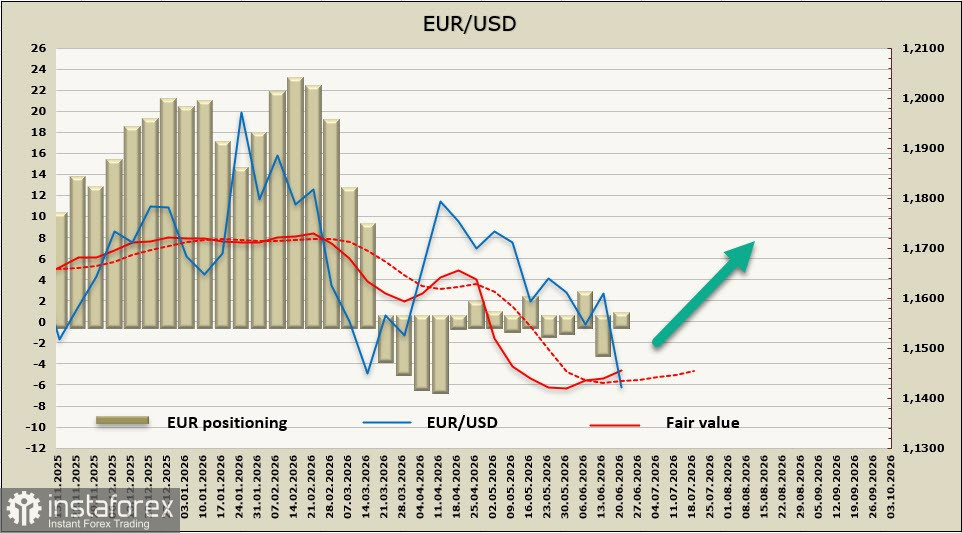

The high volatility in currency markets following the Fed meeting and the strengthening dollar may be short-term, but there is no confidence in that. In any case, we must consider that the ECB's position appears markedly weaker compared to the Fed's, and it will take time for the EUR/USD rate to find support.

Positioning for the euro has again become neutral; the calculated price continues to rise despite the significant strengthening of the dollar.

The EUR/USD pair updated the June 2025 low on Tuesday. The short-term bearish momentum, formed after the revision of forecasts regarding the Fed's rate, appears strong and has not yet played out. The likelihood of a decline in support at 1.1277 has increased, and purchases in the current situation can hardly be considered justified. The euphoria from the end of the Gulf conflict has quickly faded, as the fundamental issues it created have not disappeared; it is entirely possible that the crisis is just gathering momentum. We consider the current decline to be short-term and are awaiting signs of an upward reversal.