Silence is golden. That seems to be the choice of new Fed chair Kevin Warsh, who refused to tell attendees at the ECB symposium in Portugal whether the Federal Reserve will raise interest rates at its next meeting. Markets took the uncertainty in stride: CME derivatives price the odds of tightening this month at under 30%.

Stock index dynamics

Major US stock indices closed mixed. Economically sensitive firms of the S&P 500 outperformed tech giants as ISM's manufacturing PMI expanded for the sixth consecutive month.

At first glance, the macro picture supports investor optimism. Manufacturing activity has been expanding for half a year — a rare pace in recent years, especially after an oil shock. Cooling input prices have removed part of the inflationary pressure that not long ago had traders fearing Fed hikes. That is how Wall Street answers the question posed since the start of summer: is the current broad?market rally too narrowly based? Cyclical stocks typically move first on such shifts, and they didn't disappoint in trading on the first day of July.

A spoonful of tar came from the ADP data. In June, the private sector added 98,000 jobs — below the expected 110,000. The equity market largely shrugged off the miss: the release came ahead of the main government employment report, and investors preferred to wait for the full picture. The weak print is a reminder that the economy's resilience still needs confirmation. If the labor market disappoints, arguments for Fed tightening will weaken — and the cyclical S&P 500 rally will be called into question.

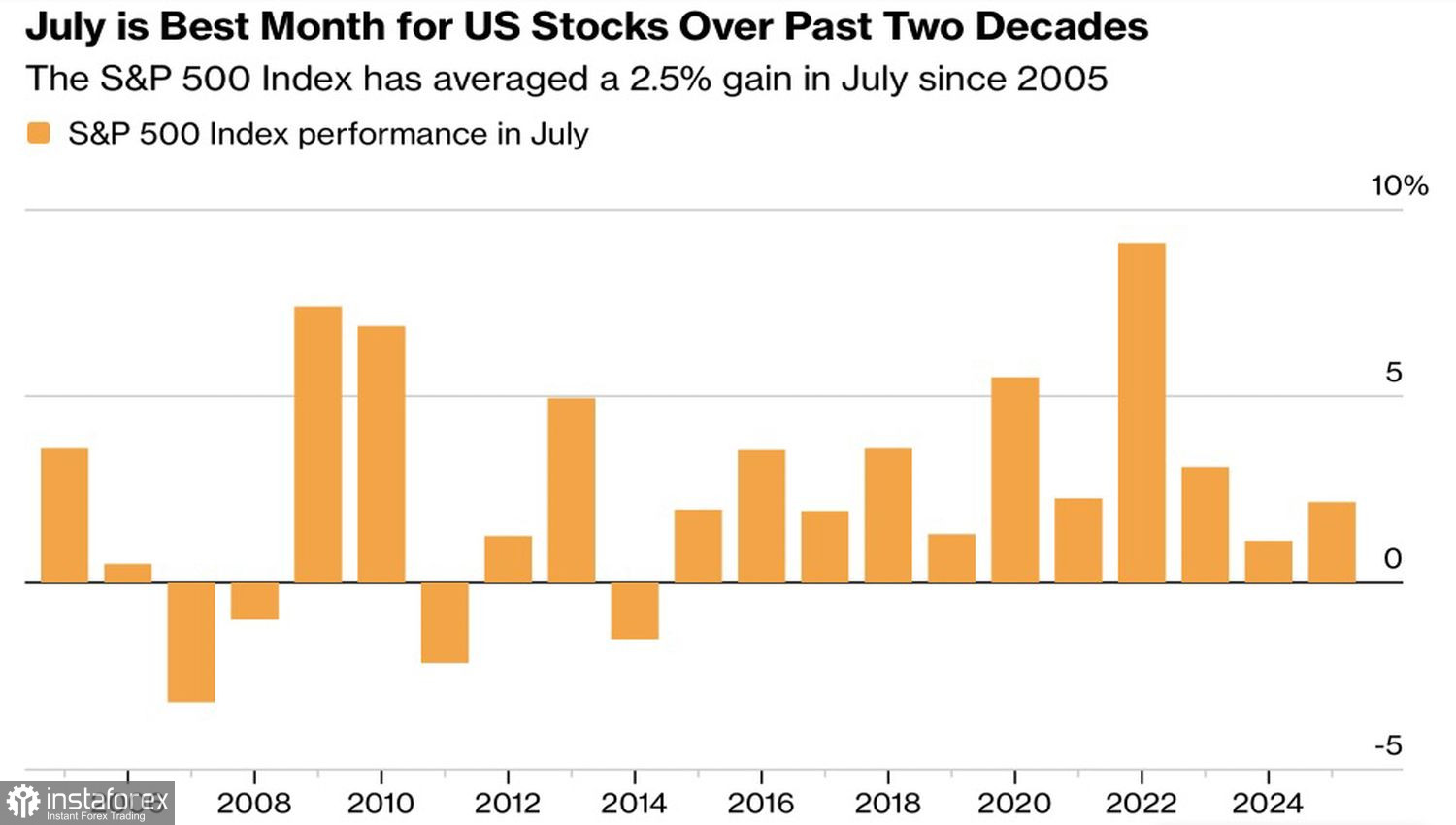

S&P 500 seasonality

Seasonality is on the bulls' side. July has historically been the best month for the S&P 500 over the past two decades: since 2005, the index has averaged a 2.5% gain — more than four times the average monthly move in the other 11 months. There hasn't been a losing July since 2014.

Still, the benign seasonality runs against fundamental risks. The fallout from the Iran war continues to affect inflation, increasing pressure on the Fed. The specter of higher rates threatens corporate profits, and the November midterms remain a wild card.

The Magnificent Seven basket lost nearly 9% in June — the worst monthly performance since March 2025. Citigroup warns that risks for the group remain elevated and that bearish flows are building both within the tech winners and across the S&P 500 as a whole. Can July's seasonal magic overcome these headwinds?

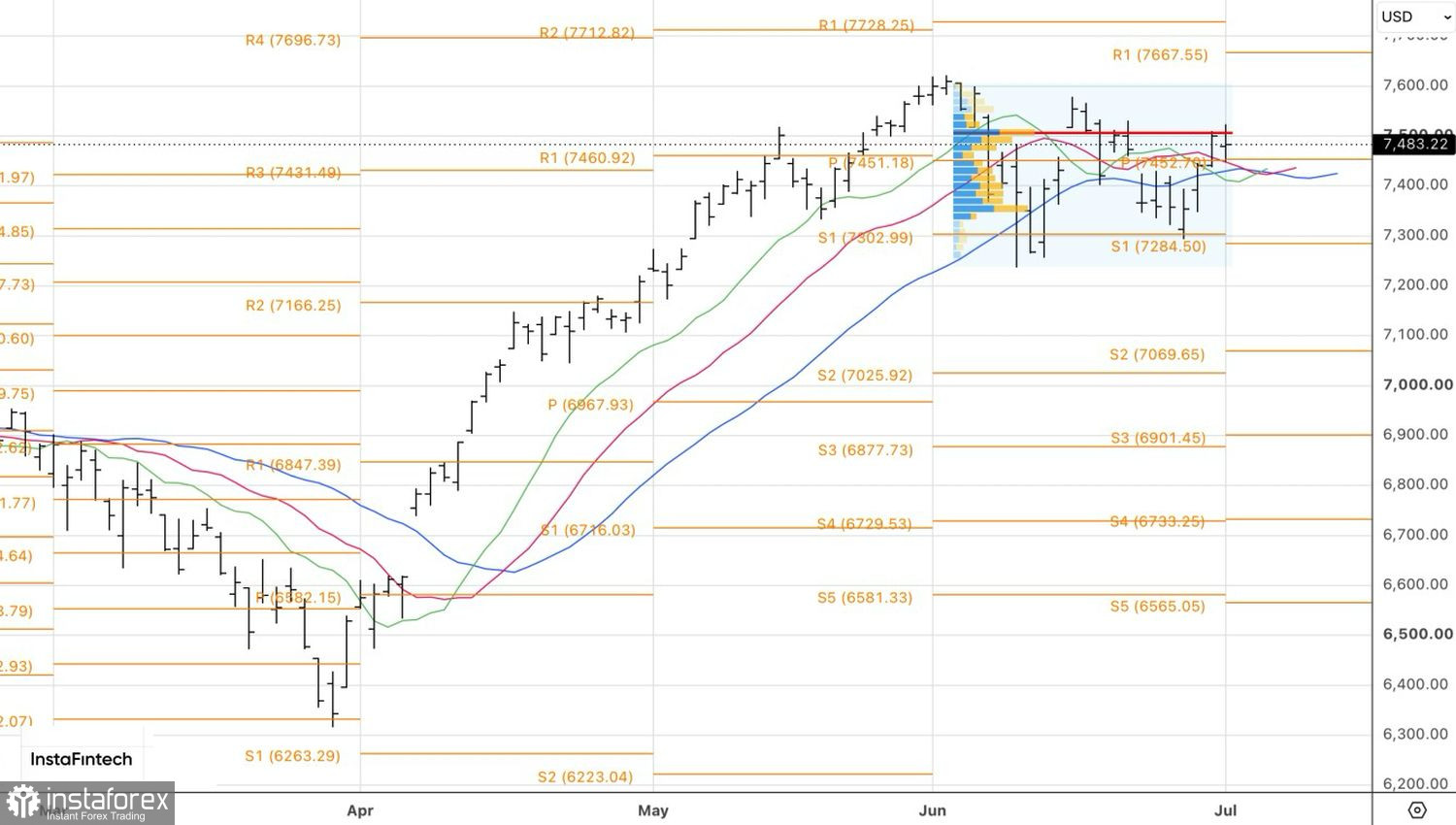

Technically, the daily S&P 500 chart showed a failed fair-value test followed by the formation of a doji bar. A break below its low at 7,445 would be a sell signal. Conversely, a rally above 7,520 would allow for adding long positions.