Japan's economy is facing renewed inflationary pressure. Tokyo's Consumer Price Index (CPI)—a key leading indicator for inflation across the country—accelerated to 1.7% year-on-year in June. Meanwhile, the core CPI (excluding fresh food) increased to 1.6%, while the broader underlying inflation measure accelerated to 1.9% from 1.6% in May, exceeding market expectations.

The Corporate Goods Price Index (CGPI) surged to 6.3% year-on-year in May, its highest level in three years, indicating that rising costs for imported energy products are being passed through more rapidly to domestic prices.

Economic growth has remained resilient so far, with GDP expanding by 2.1% in the first quarter. However, the second quarter is expected to be significantly weaker due to the highly unfavorable geopolitical environment. A recovery is likely only toward the end of the year, and only if tensions ease and global supply chains begin to normalize—an outcome that currently appears unlikely. The potential consequences extend well beyond higher inflation, including weaker real consumer demand, lower capacity utilization, and slower export growth. Ultimately, this could lead to reduced investment, representing a particularly dangerous scenario for the Japanese economy.

In April 2026, Japan's oil imports declined by nearly 66% compared with the same period a year earlier. Only aggressive efforts to diversify supply sources enabled imports to recover to around 90% of their pre-conflict level. However, the problem extends beyond crude oil. For example, shortages of naphtha caused ethylene production to decline by 37.1% in April, while energy costs surged sharply. According to the Japan Research Institute, if oil prices remain above $87 per barrel, this factor alone could trigger the beginning of a recession. A more substantial rise in oil prices could result in a 3% contraction in GDP. Japan is currently relying heavily on its strategic petroleum reserves, but those reserves are finite. As a result, the conflict in the Persian Gulf is having an increasingly significant impact on both the Japanese economy and the yen.

Financial markets expect the Bank of Japan to leave its policy rate unchanged at its July meeting, with the next rate hike not anticipated before December.

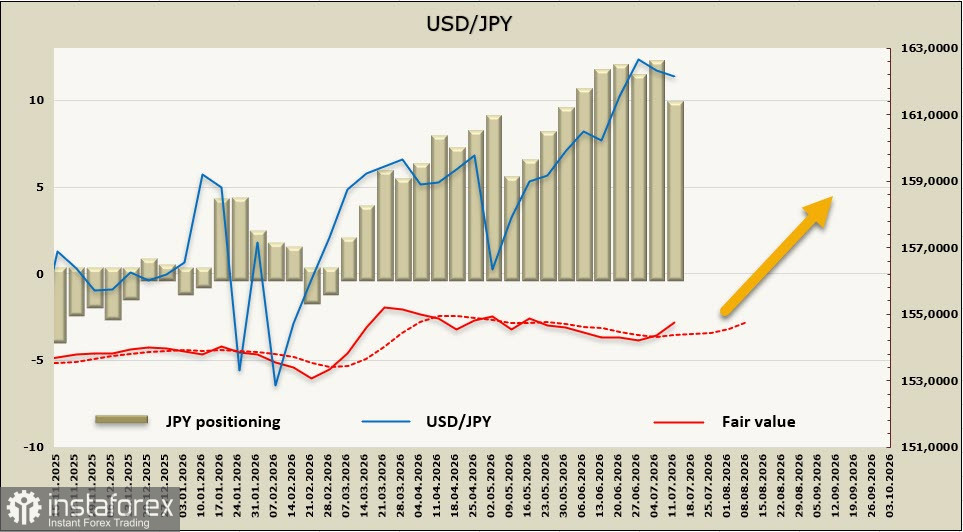

The net speculative short position in the yen narrowed by JPY 2.38 billion during the latest reporting week to JPY -9.55 billion. Despite this improvement, the estimated fair value has once again moved above its long-term average under the influence of short-term factors.

The yen has become hostage to three powerful forces: the external energy shock, deteriorating terms of trade, and the persistent interest rate differential with the United States. Although the Bank of Japan has raised its policy rate to 1.0% and remains prepared to continue normalizing monetary policy, markets are not pricing in another rate hike before December 2026.

From a technical perspective, USD/JPY is approaching a test of the 163.00 level. A sustained break above this resistance would open the way toward the 165.00–170.00 level and would almost certainly trigger a response from the Japanese authorities. From a fundamental standpoint, geopolitical developments remain the primary market driver. As long as the conflict affecting the Strait of Hormuz persists, risks remain tilted toward further yen weakness despite the Bank of Japan's increasingly hawkish rhetoric. The 163.00 level is a critical technical threshold, representing long-term horizontal resistance that coincides with the midpoint of the ascending channel in place since 2022, as well as the upper boundary of the yearly trading channel. A decisive breakout above this level would fundamentally alter the long-term outlook for the yen.