In April, investment flows shifted toward riskier assets. According to the monthly report from Bank of America, inflows into stocks turned positive, while money market funds experienced outflows. This change in investor strategy is driven by hopes for a peaceful resolution to the US-Iran conflict, as well as seasonal liquidity withdrawals for tax payments.

Data analysis from Simfund, Morningstar, and ICI shows that interest in equities has risen despite traditional tax pressures. In addition, there has been a resurgence in the fixed-income segment. On the other hand, money market funds have been losing ground since the beginning of the month, which BofA analysts attribute to the short-term need for cash to settle tax obligations.

Shift in rate forecasts

BofA economists have significantly revised their expectations for the Federal Reserve’s monetary policy. The bank now forecasts only two interest rate cuts of 25 basis points each in September and October, whereas easing had previously been anticipated in June and July.

This delay supports high yields on short-term bonds and prompts a capital rotation, with investors moving from money market funds to short-duration debt instruments. The inflow into equities has been predominantly from US issuers, while the bulk of funds in the bond market is concentrated in US Treasuries.

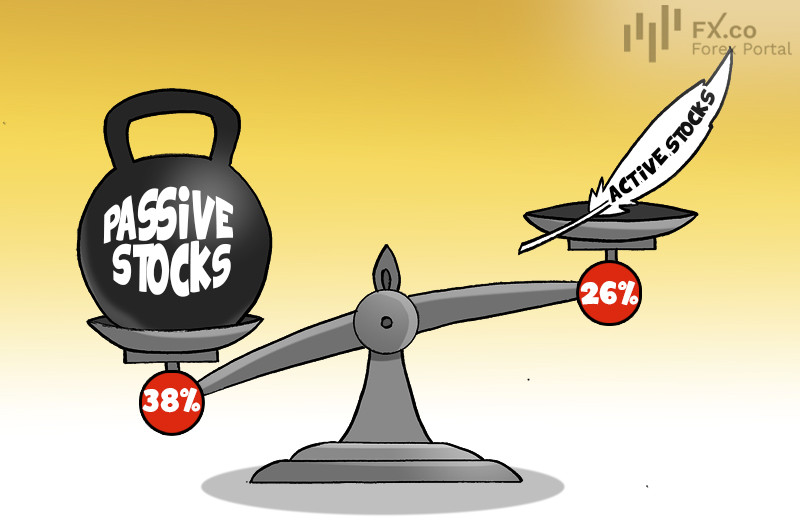

Active strategy crisis

A structural analysis of the market confirms the long-term dominance of passive investing. The share of active managers who can outperform the market over a three-year horizon remains stagnant at 27%.

BofA statistics reveal a historical shift: while actively managed equities accounted for 41% of the market in 2010, that share has now fallen to 26%. In contrast, passive instruments (index funds and ETFs) have dramatically expanded their presence from 14% to 38% during the same period, becoming the primary refuge for capital disillusioned with the performance of active portfolio managers.