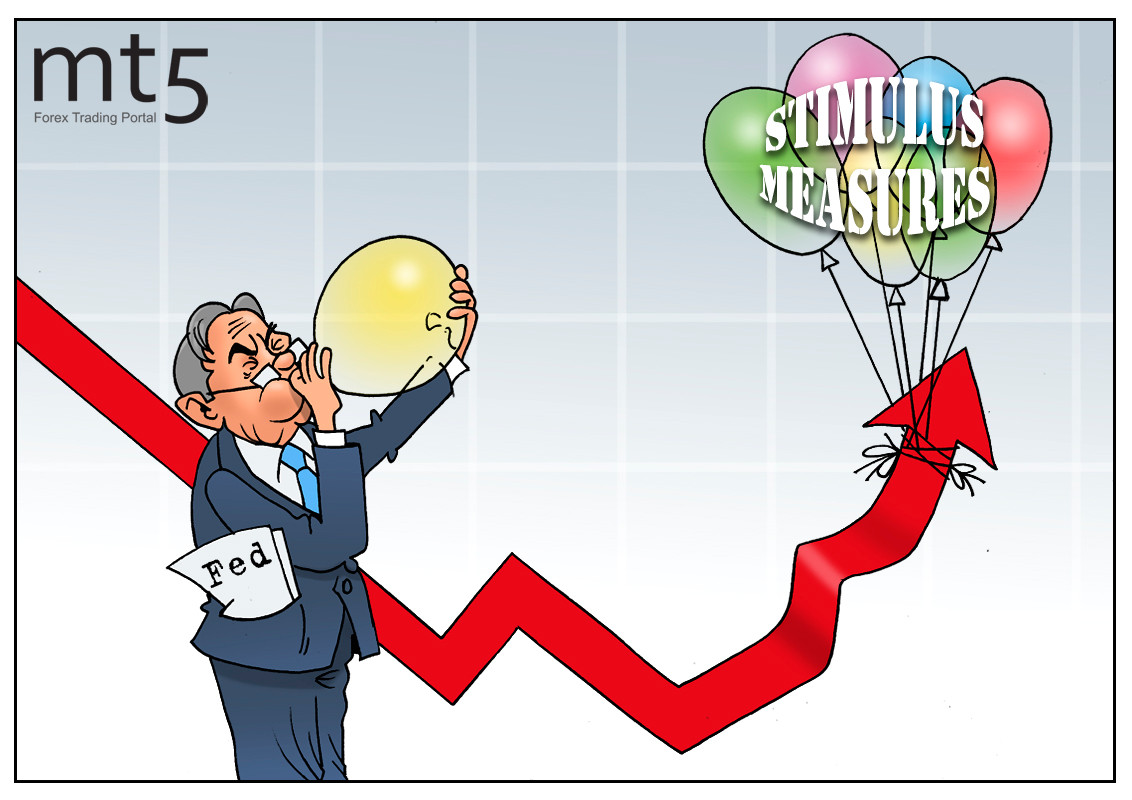

As the coronavirus pandemic is cutting the demand for oil and the standoff between Saudi Arabia and Russia continues, the United States decided to step in to save the situation. Washington announced an unprecedented array of programs to backstop the economy reeling from the virus outbreak. In an effort to prevent economic devastation, the White House rolled out a $2 trillion relief package. The mere announcement was enough for the quotes to advance. The market sentiment turned out to be more than optimistic about the stimulus measures. Oil prices rose by almost 3 percent and then went down slightly but still settled at a higher level. In addition, President Donald Trump’s comments on the “too strong dollar” also supported the markets with dollar-denominated commodities. “Oil is clawing its way higher, mainly on the back of the weaker dollar that stemmed from the Fed’s unprecedented measures. WTI crude volatility will remain high and traders should not be surprised if this rally eventually gets faded,” Edward Moya, a market analyst, commented on the situation. Still, the overall outlook for crude demand remains low due to halted production and transport restrictions in many countries. Those who wanted to buy cheap oil have already snapped it up and filled their tanks to the maximum.