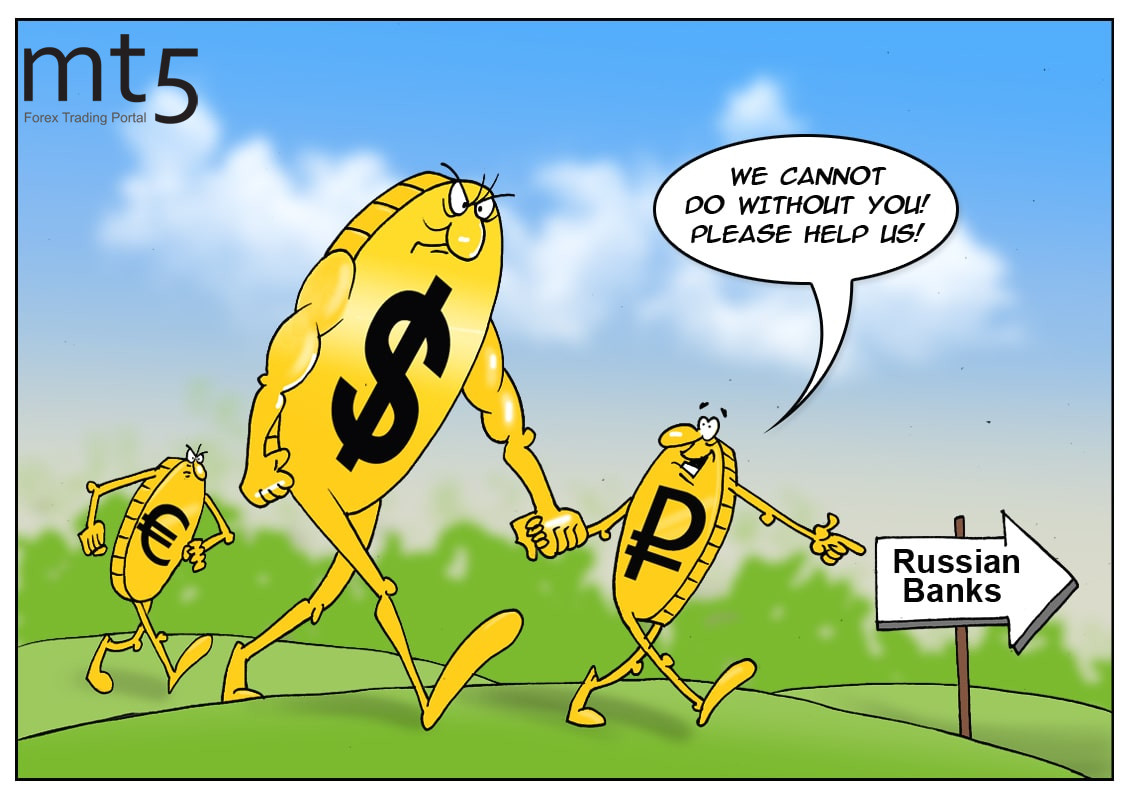

Russia could never boast of long-term economic stability, especially now in the times of uncertainty around the coronavirus-driven crisis. The Russian citizens learnt it the hard way back in the 1990s. This time, when authorities urged people not to panic over the financial well-being and safety of their savings, Russians rushed to withdraw money from banks. Amid a massive withdrawal of cash, Russian banks had to purchase their highest volume of foreign currencies in order to meet the demand. In March, Russian banks imported almost 5 billion in US dollars and another 1 billion in euros. The volume of dollars bought in March was almost 9.6 times higher than the amount imported in February. Earlier in April, a surge in demand for foreign currencies came after the ruble tumbled amid the oil price war. Today, people are closing both the ruble and foreign currency accounts. According to Russia’s Central Bank, around 315 billion rubles and more than 5 billion US dollars were withdrawn from bank accounts in March, a record amount over the past 10 years. Besides, Russian President Vladimir Putin announced a tax on bank deposits of more than 1 million rubles and on gains from debt securities. The new tax will be imposed only in 2021, but customers prefer to withdraw their deposits in advance.