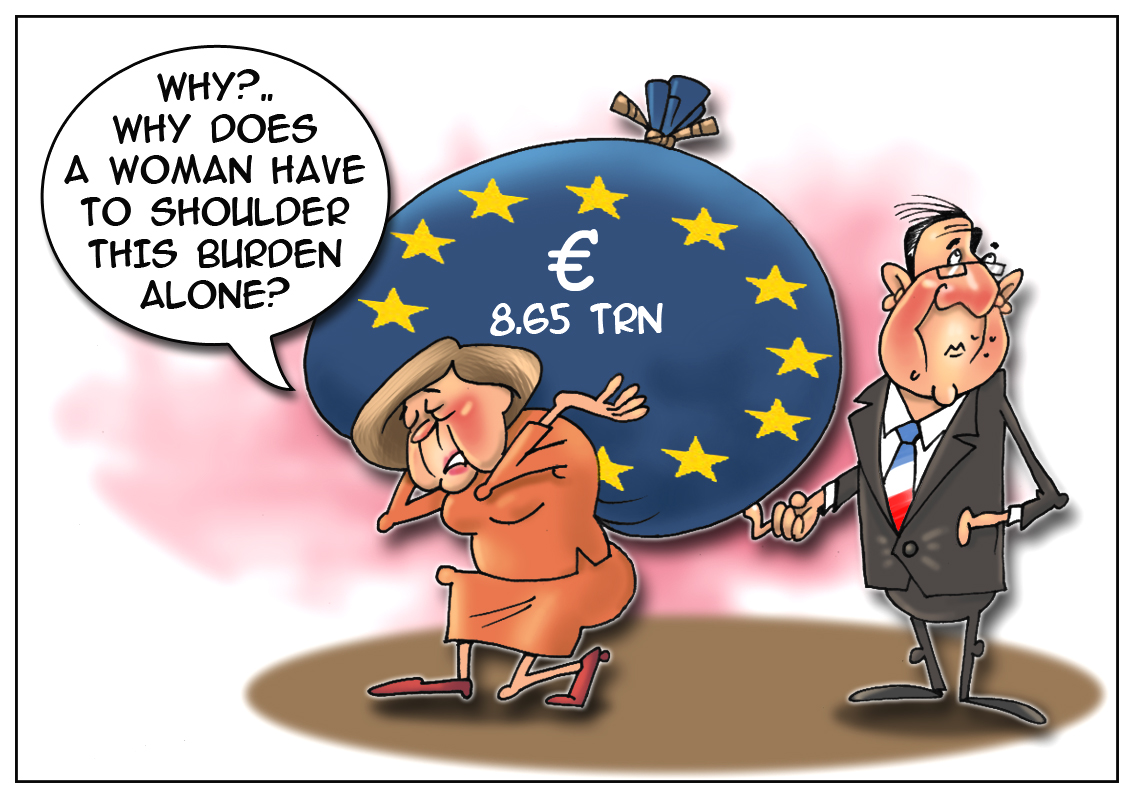

The U.S. heavy debt problems made other countries draw the lesson from this and check out their own debt warrants. As a first step, the EU countries decided to deal with the total debt amount. The reports show that the composite official debt of the eurozone states reached €8.65 trillion. When figuring out this amount as a ratio to Gross Domestic Product, it comes out at 93.4% from the annual GDP value. Although, according to Eurostat statistical agency, the European countries’ debt burden accounted for nearly 90% of GDP several months ago. After the overall data had been released, debentures of each country were assessed separately. The first rank in terms of cash assets loans obviously belongs to Greece; its indebtedness makes 169% of GDP. The next rank is taken by Italy with 133.3%. Portugal’s debt is 131.1% of GDP. Ireland occupies the fourth rank having the debt of 125.7% of the annual GDP. The most abrupt spike of the debt burden showings has been recorded in Cyprus. Its government debt jumped from 87.5% to 98.3% instantly as a result of overdue loans from long-time business partners from the eurozone and the International Monetary Fund. In contrast, Germany stands out among debtors with adverse credit records. Germany managed to bring its debt under control and even to reduce it by 0.7% to 79.8%. Once again, Germany proved itself as a reliable lendee. Meanwhile, Spain’s debt status is much worse. The national debt is going on rising, despite the government is taking efforts to cut public expenditures. In June 2013, the debt hit record high of €942.8 billion that corresponded to 92.2% of GDP.