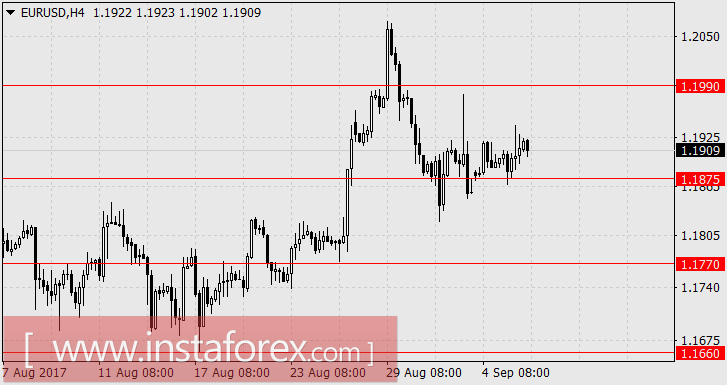

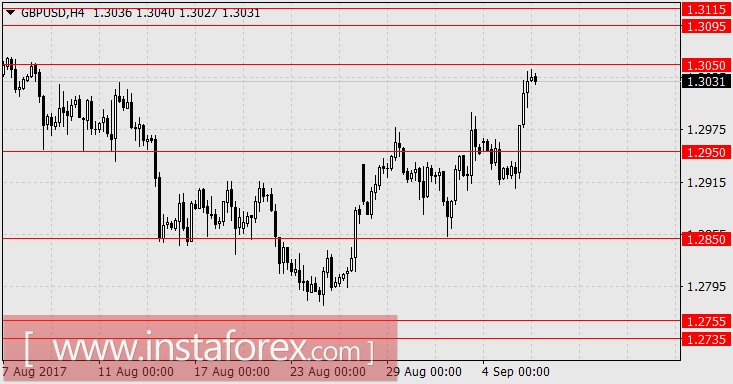

EUR / USD, GBP / USD

Unfortunately, it was misguided that there is no impulse in the strengthening of the dollar from American traders on Tuesday. Instead, the euro and the pound began its recovery against the European economic data during the start of the London session. Retail sales in the euro area for July fell by 0.3 percent against the forecasted -0.2 percent. The final estimate of the Euro zone's PMI services for August declined from 54.9 to 54.7 while the British PMI Services Index dropped from 53.8 to 53.2. Later in the evening, the U.S. data on factory orders in the July estimate came down -3.3 percent which is the forecast level and increased the growth of other dollar currency pairs. In the speech of Lael Brainard, caution was conveyed in choosing the interest rate hike. However, she confirmed the readiness of the Fed to reduce the balance. Robert Kaplan also came forward with the same theses but not without the influence of the "North Korean factor" and the impending new hurricane "Irma". The main US stock indexes lost about 1.0 percent. The U.S. government bonds were actively bought as the yields on 5-year securities fell from 1.740 percent to 1.638 percent. The probability of a December rate hike increased to 42 percent.

Apparently, speculators will be active until the announcement of the ECB monetary policy decision on Thursday. Today, the macroeconomic data could contribute to this activity. The volume of industrial orders in Germany for July is expected to increase by 0.2 percent. Retail sales in Italy are expected to decline by 0.2% but this index is not that relevant. Expectations on the U.S. data are set against the dollar. The trade balance for July is projected at -44.6 billion dollars against -43.6 billion in June. Business activity in the service sector from Markit's final estimate for August is projected to decrease from 56.9 to 56.8. The estimate of Non-Manufacturing PMI from ISM is still expected to increase to 55.8 from 53.9. At 18:00 London time, the "Beige Book", a consolidated report of the regional branches of the Federal Reserve for economic districts, will be published.

The foreign policy background for the dollar is becoming unfavorable. The White House is preparing a set of new sanctions against the United Nations and the DPRK, which China opposes. This could worsen the relationship of U.S. with China and Russia as they also oppose sanctions.

The euro will most likely rise to 1.1990 while the pound sterling ranges between 1.3095 and 1.3115.

USD / JPY

The yen did not withstand a broad weakening of the dollar. It dropped more than 90 points yesterday and continued today in the Asian session with fears of aggravating the U.S. relations with the DPRK and China. The average wage in Japan today showed a decline of 0.3 percent y / y against growth expectations of 0.5 percent y / y. In Australia, the GDP growth did not justify the forecast against the expected economic growth of 0.9% in the second quarter since it increases by 0.8% only. Stock indices are declining as expected: Nikkei 225 -0.21%, S & P / ASX 200 -0.35%, China A50 -0.82%, Kospi SEU -0.35%. Tomorrow, Japan's leading economic indicators index for July is expected to decline from 105.9% to 105.2%. On Friday, the final estimate of GDP may decrease from 1.0% to 0.7% for the second quarter. The Japanese government is working out a plan for the possible evacuation of about 60,000 Japanese citizens considering living or staying with short-term visits in South Korea in the event of a war. In the current situation, the yen is expected to be in the range of 108.05 / 25.