Today, during the Asian session, the first meeting of the Reserve Bank of New Zealand was held under the chairmanship of Adrian Orr. For several months he was the acting head of the regulators and before that he headed the Pension Fund of the country. Today he made his debut as a full-fledged chairman.

Many foreign exchange strategists eagerly awaited his speech at the end of the May meeting of the RBNZ. None of them doubted that the regulator would leave the parameters of monetary policy in its previous form, but some market participants had hope for some tightening of the rhetoric of the head of the Central Bank.

Let me remind you that the predecessor of Adrian Orr, Graham Wheeler, was extremely soft on the monetary policy, especially over the past three years. Since 2015, the RBNZ interest rate has been gradually declining, from 3.5% to the current 1.75%. Willer was a supporter of a weak "kiwi" and with enviable regularity, he exerted verbal pressure on the national currency. In addition, he loosened the terms of monetary policy, despite the risk of "overheating" the real estate market in the country. Persistently professing the dovish policy, he tried to influence the housing market with the help of other measures (in particular, regarding the determination of the loan amount to the value of the pledge).

In other words, after several years of extremely mild monetary policy, the New Zealand Central Bank has a chance to change course - at least in the distant future. Some experts did not rule out the possibility that the new head of the RBNZ would declare a way to normalize monetary and credit policy, despite the continuing risks.

However, today all the hopes of the New Zealand currency bulls have collapsed. Adrian Orr did not only preserved the "dovish" mood of his predecessor but even surpassed him in terms of voiced pessimism. Firstly, he said that he was extremely surprised and disappointed with the weak growth in the level of wages in the country. Secondly, he expressed dissatisfaction with the rate of inflationary growth and worried about the weak confidence of businessmen in the business environment. Among the main risk factors, he mentioned US bonds, the yield of which persists at multi-year highs of 10-year treasuries has once again broken the 3 percent barrier.

The head of the RBNZ and China were Disappointed in the context of a possible slowdown in the global economy. By the way, the data published on Chinese inflation really disappointed the market today. The indicator did not even reach a sufficiently weak forecast, reaching 1.8%. In annual terms, the indicator has been slowing down for the second month in a row, and this fact signals an "alarm bell" for the markets.

However, he head of the New Zealand Central Bank addressed China casually, focusing on attention to inflationary growth. Assessing the prospects for a monetary policy, he stressed that in this issue "the doors are up and down - everything depends on the further development of the situation."

In other words, Adrian Orr did not exclude the possibility of lowering the interest rate in response to a decline of the consumer price index. Inflation has been falling for several quarters in a row: the latest release came out at 1.1% amid the strengthening of the labor market. Therefore, if you project this trend with the words of the RBNZ head, the likelihood of mitigating monetary policy does not look so incredible. Although even at the beginning of this year, experts allowed only an alternative scenario, albeit with an open implementation date.

In addition, Adrian Orr noted a downward trend in the real estate market. The decline in house prices in a certain sense "unties the hands" of the regulator's members regarding the easing of the terms of the credit policy. This is a very indirect factor, but in conjunction with the other theses of today's Orr speech, the overall picture looks quite negative for the national currency.

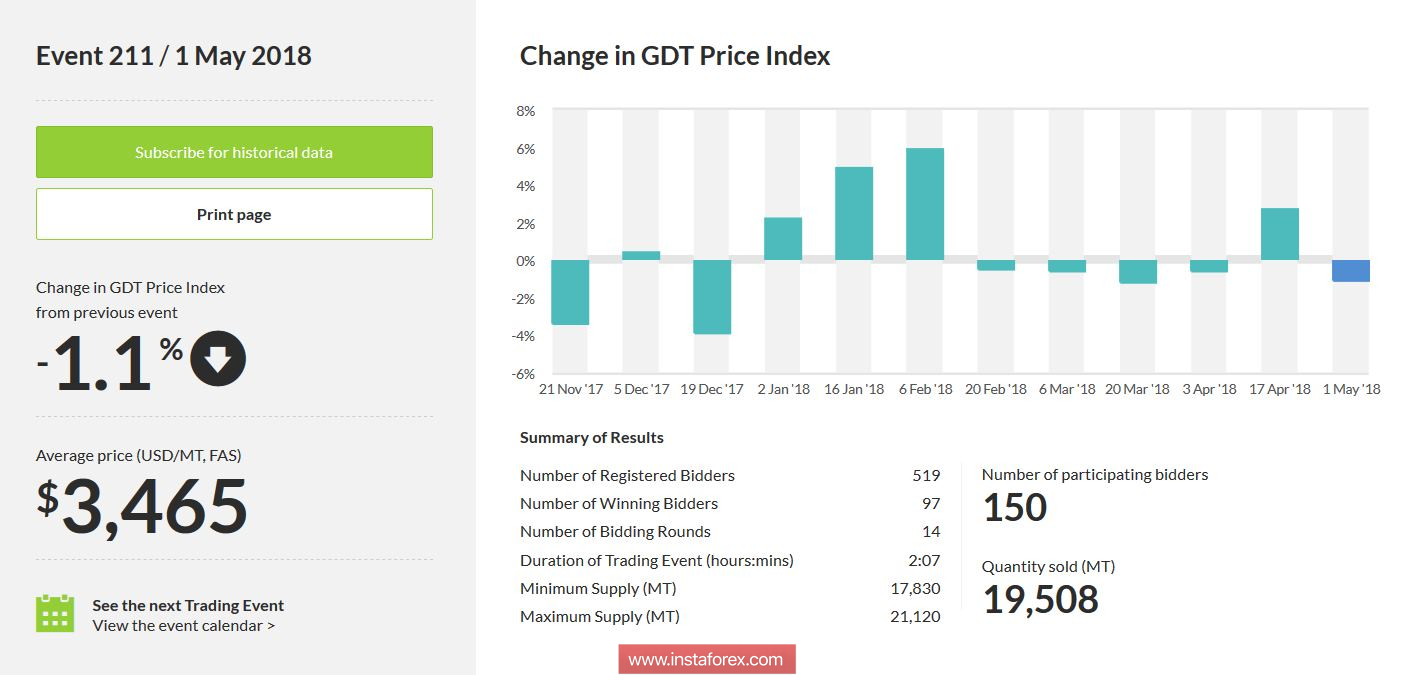

It should also be noted that in addition to the slowdown of inflation and sluggish GDP growth It may be disappointing and less significant, but it is still significant for New Zealand indicators. In particular, the price index for dairy products again found itself in the negative area. Since the end of February, the index was below zero, but it unexpectedly showed growth on April 17. he first auction in May was to confirm or refute this trend.

Alas, the results of the Day auction in May were negative. The index again went into the negative area due to the reduction in the price of dried whole milk and milk fat. As known, the dairy sector is strategically important for the New Zealand economy, so the above trend exerts additional pressure on the NZD/USD pair.

Thus, the overall fundamental background for the New Zealand currency remains negative. The new head of the RBNZ Adrian Orr showed himself to be a supporter of a soft monetary policy, allowing the probability of a rate cut. The remaining fundamental factors also play against the New Zealander. This circumstance intensifies the pressure on NZD/USD pair against the background of the U.S. currency growth.

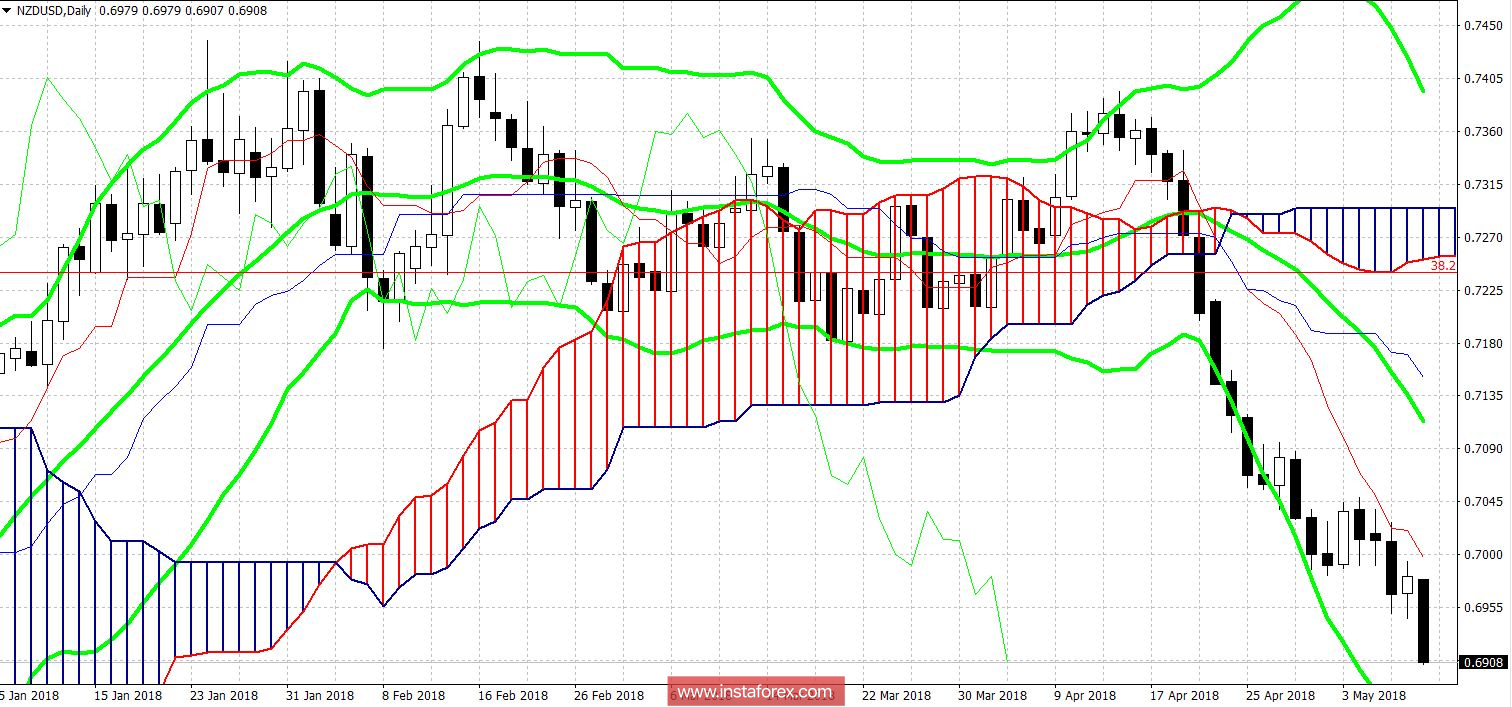

From the technical point of view, the priority is for the southern movement of the pair. On all the "higher" timeframes, the Kinko Hyo indicator demonstrates a bearish signal "Line Parade", and the price is located between the middle and Bollinger Bands at the bottom lines of the indicator n the monthly chart, which coincides with the one and a half-year price minimum.