As hysteria continues in Europe regarding the COVID-19 "Omicron" strain, which is manifested in strict isolation measures in the UK, there is a pullback of concerns in the US in the wake of statements by epidemiologists that currently existing vaccines against this infection block viral infection.

These positive sentiments are manifested in a three-day growth in the stock market in America, which can fully develop into a longer Christmas rally. If the topic of the ill-fated "Omicron" has almost disappeared from the headlines of the business media, then discussions of the Fed's upcoming monetary policy measures are increasingly beginning to appear following the results of the meeting, which will begin on December 14 and end on December 15.

There is a concern in the market about what the American regulator will do with the course of monetary policy. If earlier the consensus forecast was based on expectations of the start of the process of raising interest rates in the middle of next year, then the latest statements by J. Powell, the head of the Central Bank, told the banking committee in the Senate that the bank could accelerate the process of reducing asset repurchases by reducing volumes not by $ 15 billion, as stated, but by $ 30 billion, then this would only strengthen the sale of US Treasury government bonds, which would push the dollar exchange rate up. Investors are afraid of this, or rather, of the unknown.

In recent years, confidence in the Federal Reserve has been shaken in the markets. The regulator, represented by its leader, as well as the heads of the Federal Reserve banks, repeatedly made forecasts and made plans for the future development of the national economy and the course of monetary policy, which either were not justified or were not implemented, plunging markets into a state of uncertainty, and this led to an increase in volatility. And now investors expect clarity from the Central Bank following the results of the meeting in the timing and pace of the likely rate increase. And here an important role will be played by the publication tomorrow on Friday of November data on consumer inflation.

It should be reminded that both the general inflation and the base inflation are expected to grow in annual terms, but on the contrary, their monthly values should demonstrate some slowdown in growth.

Why is this data important for the Fed and, ultimately, for the market?

They will help the Central Bank to understand the dynamics of inflation and, perhaps, somehow imagine what needs to be done to curb it. But again, let's pay attention to the fact that these figures will not be enough to make a final decision. Earlier, we pointed out that in order to finally decide for himself when and at what rate to raise rates, he needs data for at least three months. That is why previous reviews mentioned the January meeting of the regulator, which will take into account the inflation values for the last two months of autumn and December. If indeed inflationary pressure begins to gradually fall, then in this case we should expect a later start of rate hikes next year, for example, in late summer or even in autumn. But if, after a likely pause in growth in November, it increases in December, then we expect that rates will still be raised in the first quarter of 2022.

For the market, the slowdown in inflation and the postponement of rate hikes in the timing will lead to a new wave of demand for risky assets and a weakening of the US dollar. At the same time, increased inflationary pressure will weigh down stock indexes and stimulate the appreciation of the dollar.

Forecast of the day:

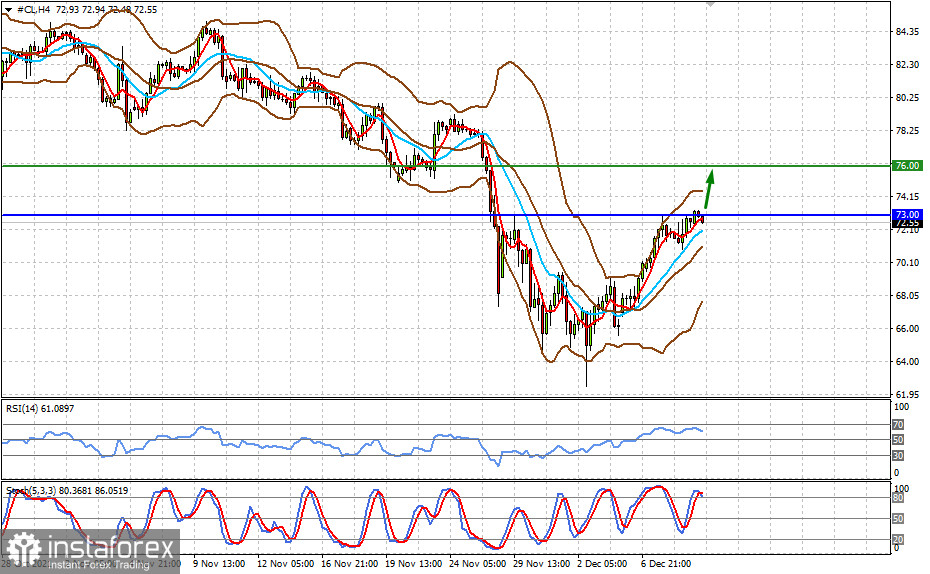

WTI crude oil prices are trading below $ 73.00 per barrel. High demand for this product against the backdrop of winter and the expectation that OPEC+ will not change their approach to politics in the future, will stimulate price increases. In this regard, an increase above the level of 73.00 will lead to a price growth to 76.00.