The US retail sales data for June sent mixed messages. The headline retail sales figures came in weaker than expected at 0.2% month-on-month (compared to a forecast of 0.5%), but historical data was revised higher. However, sales of core goods that impact GDP came in stronger than expected at 0.6% month-on-month (compared to a forecast of 0.3%).

Overall, the data suggests that real consumer spending increased by approximately 1% on an annual basis in the second quarter, significantly lower than the 4.2% growth seen in the first quarter.

Industrial production disappointed expectations, posting a decline of 0.5% month-on-month (compared to a forecast of 0.0%), with manufacturing output down by 0.3% month-on-month. Given the well-known weakness in the manufacturing sector, there wasn't much to look for in these numbers.

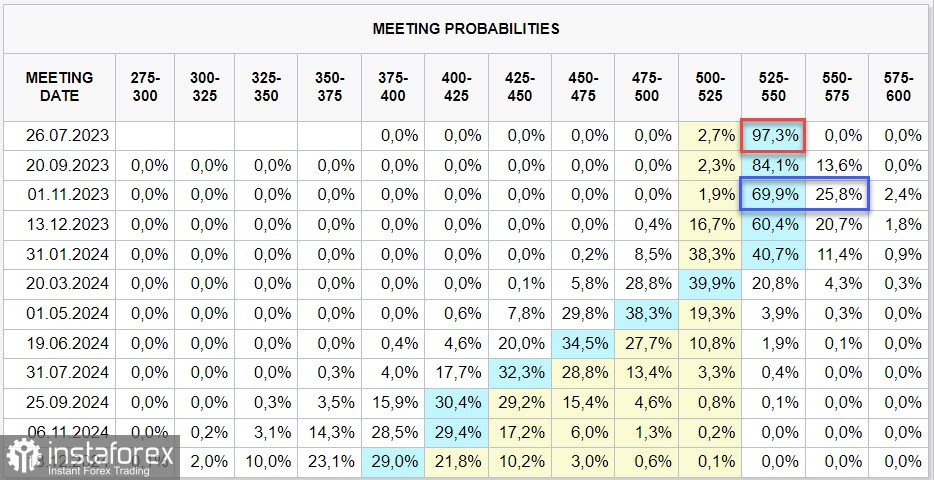

Following the release of the data, the Atlanta Fed's GDPNow estimate for the second quarter was revised slightly higher to 2.4% on an annualized basis, up from 2.3% last week. The forecast for the Federal Reserve's rate hike implies nearly 100% certainty of a rate hike next week and a small probability of another hike in November, but considering the deceleration in US inflation dynamics, the central bank will likely hit its peak level of interest rates in July.

History shows that markets quickly ignore the peak of the rate cycle and push the US dollar down, and the USD sell-off from last week may indicate that the process has already begun. If that's the case, the CFTC report, which will be released on Friday, is expected to show an increase in short positions on the dollar, leading to a revision of the long-term forecast towards further weakening.

USD/CAD

The Consumer Price Index in Canada tumbled to 2.8% in June from 3.4% in May, and the core index fell from 3.7% to 3.2%, both figures significantly below expectations. Bank of Canada Governor Tiff Macklem had already stated last week that the last part of the disinflation process (from 3-4% to 2%) will take time, and the latest reports confirms his view.

The slowdown in inflation may exert some pressure on the CAD, similar to what happened with the US dollar last week, but it is unlikely to be as strong since the decline in inflation was expected and partially reflected in the quotes. The Bank of Canada currently maintains a hawkish approach and confirmed its readiness to continue raising interest rates at its latest meeting.

The BoC rate forecast has remained largely unchanged, with a 62% probability of another rate hike by the end of the year.

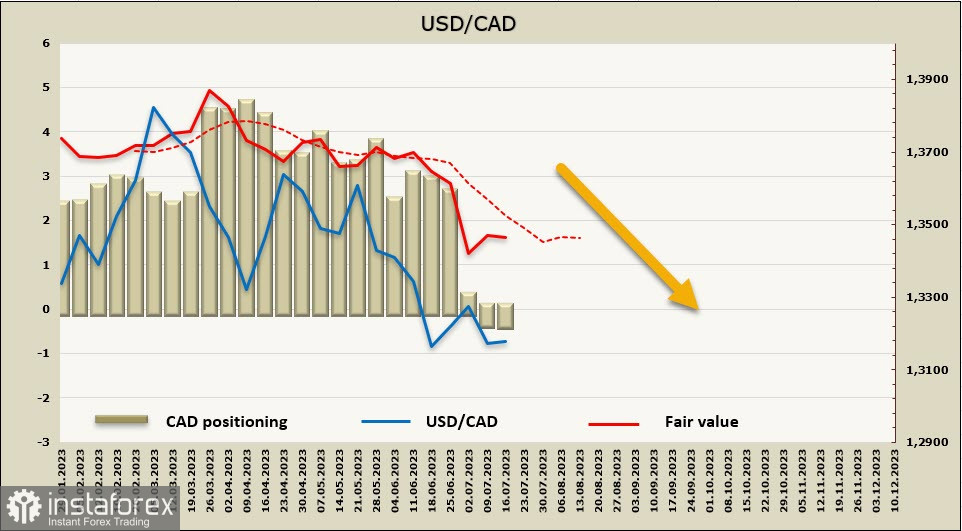

The weekly change in CAD was minor (-6 million), with a net cumulative position of +336 million, which is close to the neutral level. The calculated price is below the long-term average, indicating a downward direction.

In the previous review, we identified the nearest target as the channel boundary at 1.3040/60. Weak activity prevented the pair from reaching the target, but it still managed to reach a local low, and the attempted rally faced resistance near the recent support level at 1.3220. We expect the pair to fall, and the target is adjusted slightly lower to 1.3000/30. From a technical perspective, this is where a strong support area is located.

USD/JPY

Ahead of the Bank of Japan's meeting next week, BOJ Governor Kazuo Ueda stated that the Bank continues to maintain an ultra-soft policy, based on the view that it is still far from achieving its inflation target. It is implied that if the Bank's inflation forecasts are not significantly revised upward, its ongoing monetary easing will continue.

The yen's exchange rate is largely influenced by whether any changes will be made to the yield curve control (YCC) policy at the upcoming meeting in late July, as well as the approaching agreement of major corporations on a significant increase in wages, which will have a strong impact on inflation expectations.

Nikkei wrote in an editorial article that Deputy Governor Shinichi Uchida has so far ruled out a review of QQE, citing that "it is a good way to maintain quantitative easing." Therefore, we don't expect the central bank to take any specific actions at its July meeting. Considering that speculation about possible adjustments to the YCC in July had a strong impact on the appreciation of the yen exchange rate, we can assume that the Japanese currency is likely to weaken as these expectations are not realized.

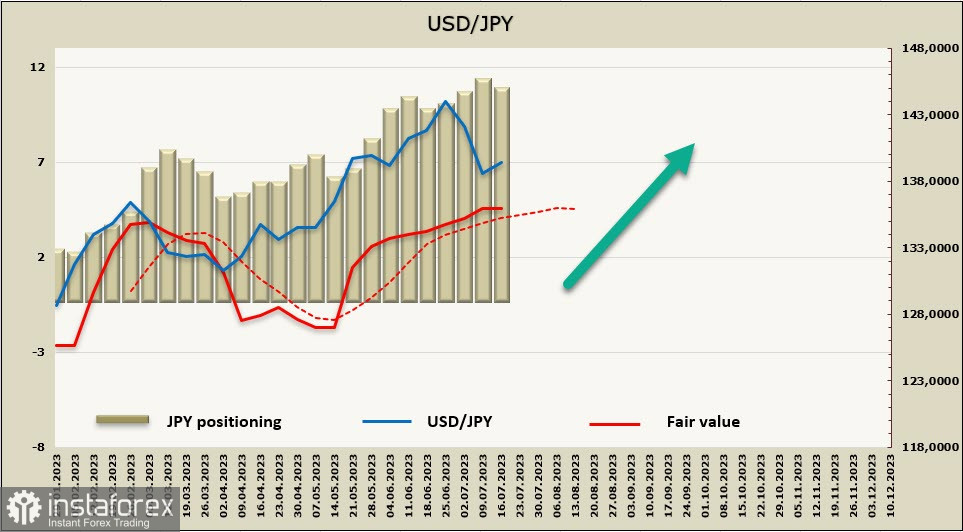

The net short position on the yen increased by 233 million to -10.436 billion, positioning remains confidently bearish with no signs of a reversal. The calculated price barely reacted to a strong corrective movement, indicating the potential for a sustained bullish trend.

USD/JPY failed to hold below the support level at 137.80, and we expect the uptrend to resume from current levels. What holds this back is the expectation of the broad US dollar weakness after the end of the Fed's rate hike cycle. If these expectations materialize (which is the prevailing scenario in the markets), then the USD/JPY pair will enter a balanced state, with trading predominantly within a sideways range.