The Australian dollar continues to dive against the U.S. currency, updating new price lows. Yesterday, AUD/USD bears marked the 0.6457 level—the lowest value of the Aussie since November 2022. Buyers are trying to catch profits on modest corrective pullbacks, but it is an extremely risky undertaking, considering the strength of the downward wave.

Today's downward impulse is driven by several fundamental factors. Firstly, the dovish RBA minutes; secondly, the decrease in the Australian wage price index; thirdly, China's disappointing macroeconomic data. Meanwhile, the U.S. dollar index is under background pressure—this indicates that the driving force behind the decline in AUD/USD is the Australian currency.

RBA Minutes

Let's start with the RBA minutes. Recall that at the end of the August meeting, the Reserve Bank of Australia surprised traders with a dovish move: contrary to the expectations of most experts, the regulator did not raise interest rates, keeping all monetary policy parameters unchanged. In the accompanying statement, the regulator indicated that inflation in Australia, although decreasing, "remains too high." In this context, the central bank noted that to ensure the return of inflation to the target level within a reasonable time, "some further tightening of monetary policy" might be required, but corresponding decisions would be taken from meeting to meeting.

The published minutes of the August meeting, for the most part, reiterated already voiced statements. The document states that the need for further rate increases will depend on "incoming data and changing risk assessments." We also learned from the minutes that the Board of Governors considered two scenarios: a rate hike of 25 basis points or keeping it at the current level. As RBA members noted, the arguments for maintaining the status quo were more compelling. Another significant phrase in the minutes draws attention—the current rate level (4.1%) "provides a reliable path back to the target inflation level." Arguably, this is the key message of the published document, reflecting the overall sentiment of the Australian regulator members.

However, traders ignored the phrase that the central bank might tighten monetary policy in the future. This wording has taken on a formal (routine) character. The central bank left the door open for further rate hikes but effectively relegated this decision to extraordinary measures. Therefore, the RBA minutes published today were quite reasonably interpreted by the market as unfavorable for the Australian currency.

Wage Price Index

Simultaneously with the RBA minutes, a crucial macroeconomic data was published in Australia—the Wage Price Index (WPI). It is another indicator of inflation and a measure of the "overheating" of the labor market. High growth rates of this indicator support the Aussie in anticipation of rate hikes. It is believed that the Reserve Bank pays close attention to this indicator when discussing the fate of the interest rate.

In annual terms, the index had shown an upward trend for a long time (since the first quarter of 2021), reaching its peak (3.7%) in the first quarter of 2023. According to data released today, in the second quarter of this year, the indicator unexpectedly slowed down, minimally decreasing to 3.6%. Although the decline is minimal, the important thing is the fact of the decrease itself, following many months of consecutive growth. Note that June Consumer Price Index in Australia was also in the red at 5.4% (an annual minimum). In the second quarter, CPI slowed to 0.8% (compared to a forecasted drop to 1.0% after growing by 1.4% in the first quarter), the weakest pace of growth since 2021.

Overall, recent inflation reports increase the likelihood that the Reserve Bank of Australia will once again maintain a wait-and-see attitude next month, just as it did at the August meeting. The RBA minutes published today only reinforced the confidence in this scenario.

Disappointing News from China

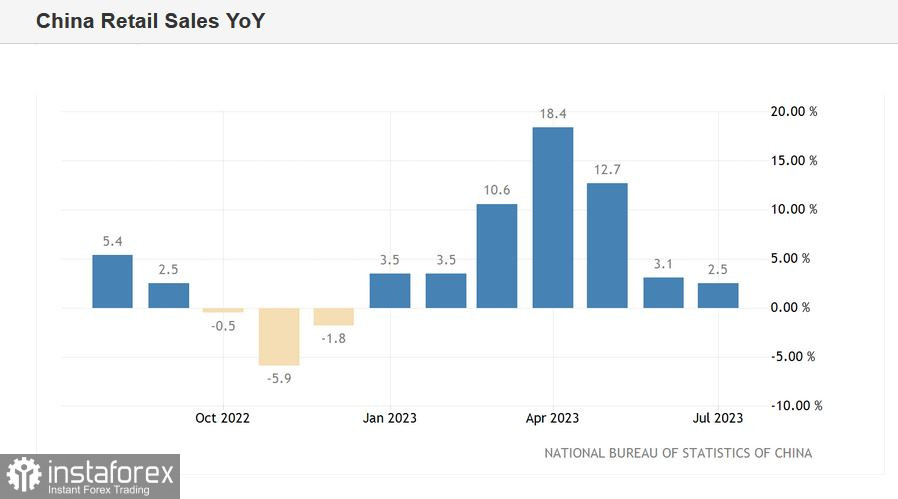

The Australian dollar faced additional pressure from news out of China, indicating that the July retail sales and industrial production data in China had deteriorated, and quite significantly at that. It was revealed that retail sales in China grew by 2.5% year-on-year in July, while most experts had predicted an increase of 4.8%. In June, sales had grown by 3.1%, indicating a downward trend.

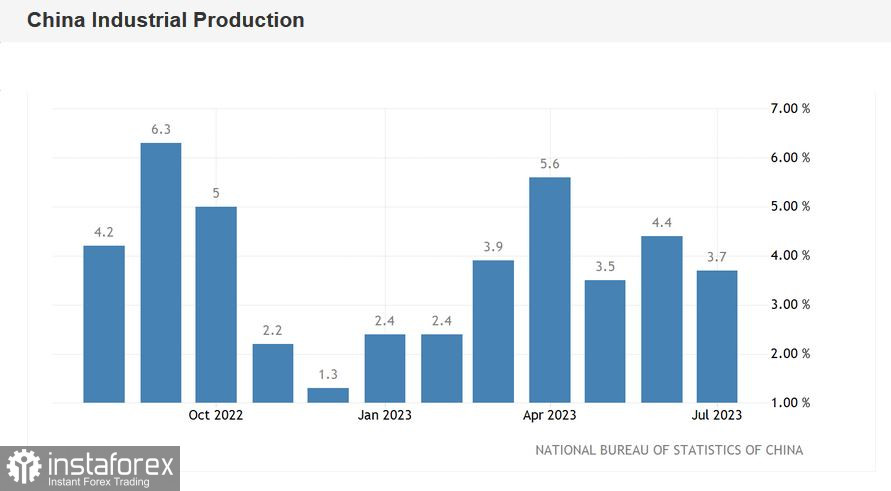

Industrial production in China increased by 3.7% year-on-year. This figure was also in the red, as the forecast had been at 4.5%. In June, industrial production had grown by 4.4%.

Another disappointing metric was the volume of investments in fixed assets in July, which grew by 3.4% since the beginning of the year, while the forecast had been 3.8%.

The Aussie negatively reacted to the macroeconomic statistics block published in China.

Conclusions

The prevailing fundamental backdrop supports further declines in the AUD/USD pair. The downward trend is not only due to the overall strengthening of the greenback but also the weakening of the Australian dollar. A decrease in hawkish expectations regarding the Reserve Bank of Australia's future actions, along with negative macroeconomic news flow from China, put pressure on the Australian currency.

From a technical standpoint, the AUD/USD pair on all "higher" timeframes (from H4 and up) is positioned between the middle and lower lines of the Bollinger Bands indicator, suggesting a bias towards the downward direction. The Ichimoku indicator has formed a bearish "Parade of Line" signal, which also implies a bearish sentiment. The nearest, most significant support level is on the lower Bollinger Bands line on the daily chart, at the 0.6420 mark. Overcoming this target will pave the way towards the 0.63 level.