The US dollar continues to maintain the highs it reached on Monday; a slight pullback appears to be a technical correction rather than a sign of potential weakness.

On Tuesday, stock exchanges were trading in different directions, with Asian exchanges closing mostly lower, while Europe was in the green, and US stocks started the day near Monday's levels.

There are signs of risk appetite, reflected in the rise in oil prices and the stability of stocks, but commodity currencies are unable to gain any advantage for now.

The US ISM Non-Manufacturing Index posted an upside surprise by rising to 53.4 last month from 50.5 in December. The economy continues to demonstrate resilience in the face of high interest rates, increasing the risks and reducing the chances of the Federal Reserve lowering rates in March. The employment sub-index jumped from 43.8 to 50.5, the largest increase since January 2021.

There is still no reason to expect a downturn in the US Dollar Index; the dollar is still the market's favorite. Futures markets give a March rate cut a less than 18% probability. Moreover, the likelihood of a rate cut in May has dropped to 55%. A little more, and the market will start expecting the first cut in June, which means a revision of yield forecasts in favor of the dollar, with waning chances of further weakness.

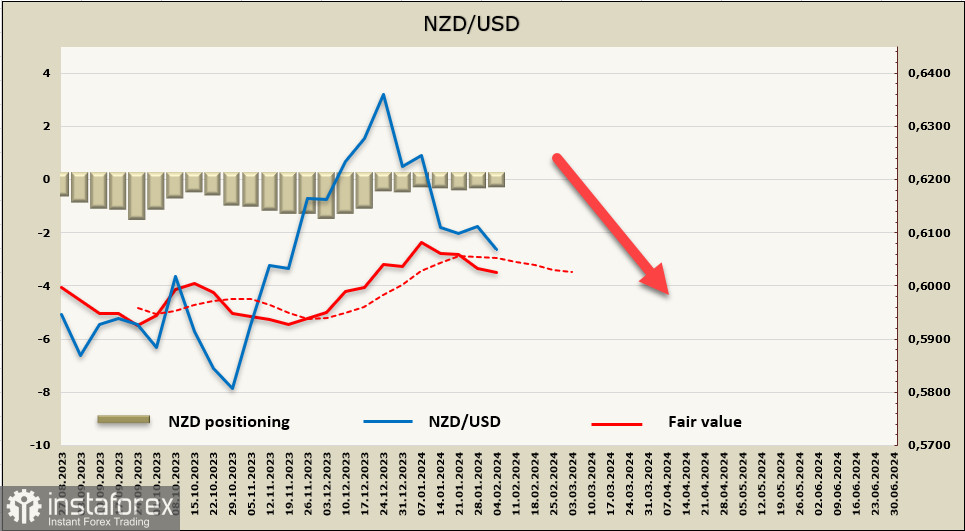

NZD/USD

The chances of the Reserve Bank of New Zealand raising the OCR have faded again as evidence of the impact of monetary policy and falling inflation accumulates. However, there's still a possibility, given the slightly hawkish tone from their chief economist last week and the high level of inflation.

Labor market data for the fourth quarter is scheduled for Tuesday. The unemployment rate is expected to increase from 3.9% to 4.3%, which is higher than the RBNZ's November forecast. While a slowdown in the economy has played a role in reduced labor demand, the growth in the labor supply, primarily through migration, is still a key factor. As the growth in labor supply continues to outpace labor demand, it is expected that wage growth, closely linked to internal inflationary pressures, will continue to slow.

Average hourly earnings are expected to decrease from 7.1% to 6.8%. If the forecast proves accurate, the chances of another rate hike will also decrease, and after the report, the NZD may fall further.

For now, it is prudent to assume that the markets are assessing the probability of another RBNZ rate hike before the start of the easing cycle in the summer. If this probability persists, the kiwi could rise from current levels. Still, if the labor market report turns out to be less inflationary than anticipated, the chances of a rate hike will approach zero, and nothing will prevent the NZD from falling further.

The net short NZD position decreased by 43 million to -64 million during the reporting week. The net positioning remains firmly neutral with a slight bearish bias. The price is below the long-term average and continues to decline.

As expected, NZD/USD attempted to consolidate below the support at 0.6057 but has been unsuccessful so far and is currently trading just above it. The rise is considered a corrective move, with the nearest resistance area at 0.6105/20, where a bearish reversal is possible. We expect bearish movement with 0.5995 as the target, where short-term support may be found. A consolidation below 0.5995 is currently unlikely, as uncertainty remains high, and there is no clear signal that the kiwi will fall further.

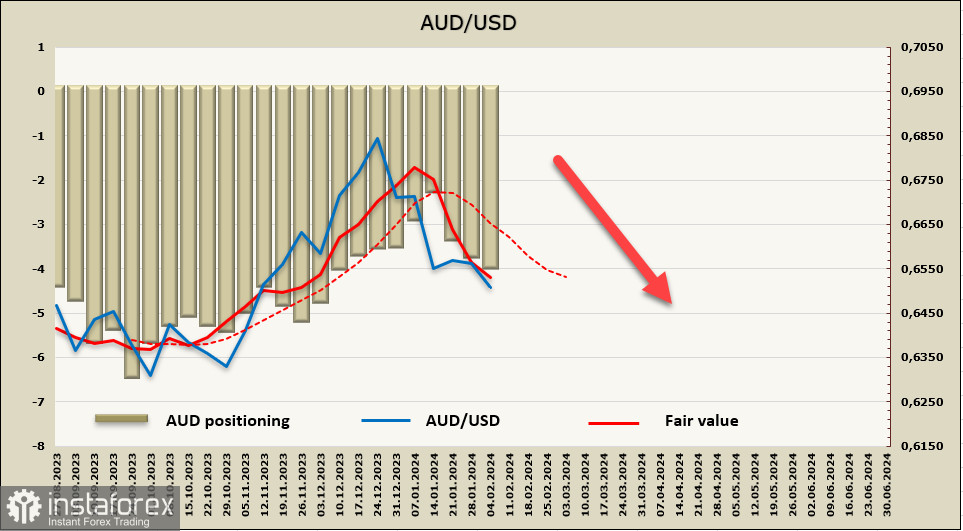

AUD/USD

The Reserve Bank of Australia, at its meeting on Tuesday, kept the interest rate at 4.25%. The accompanying statement noted that while inflation shows signs of sustained decline, it remains elevated in the services sector, and the central bank is still far from reaching the target level.

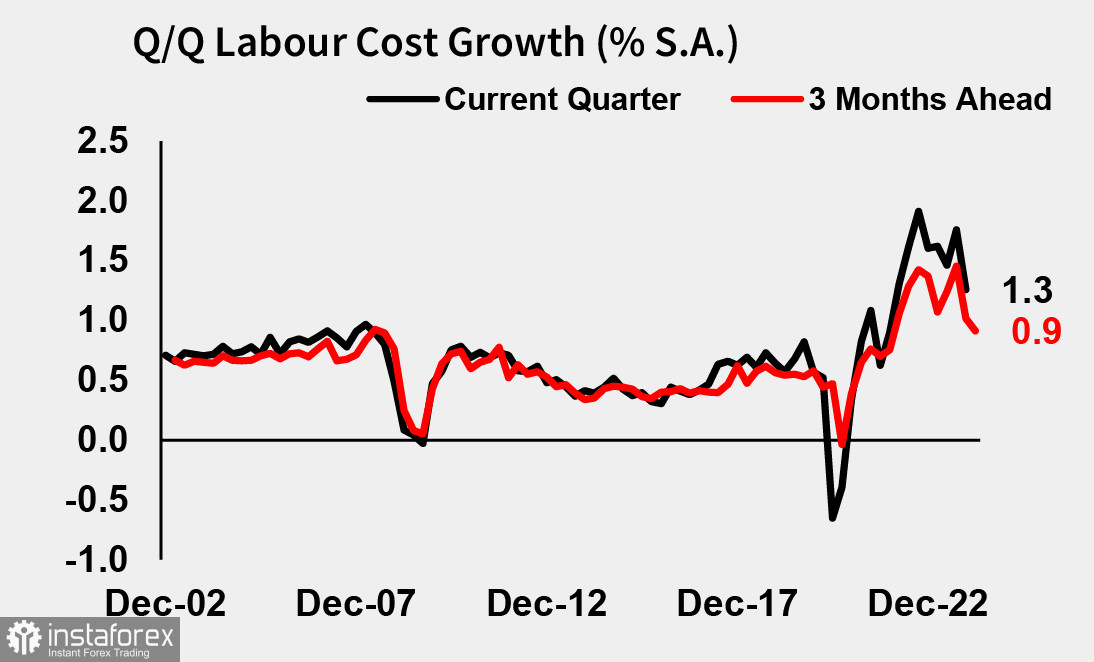

In December 2024, the market predicted a rate hike to 4.6% in February, but reality has adjusted those forecasts. Consumer inflation is steadily decreasing, and wage growth has finally started to show signs of slowing down, as indicated in the quarterly business survey.

The issue of the pace of wage growth is particularly highlighted in the survey. The price pressures receded with both input cost and output price inflation rates descending, with labor costs growth rates slowing from 1.9% to 1.3%.

Perhaps this parameter served as an additional argument for the RBA not to raise the rate again but to wait for the next report and ensure that the dynamics of inflation and wages remain positive. In any case, the RBA left the rate at the current level. However, since another hike was already priced into the aussie's quotes in December, the Australian dollar fell after the meeting and, apparently, will experience more pressure for some time.

The net short AUD position has been increasing for the third consecutive week, with the latest change being -288 million, bringing the total bearish bias to -3.849 billion. The price is steadily declining.

As expected, AUD/USD dropped below the support at 0.6527. The nearest resistance is at 0.6525, followed by 0.6550/60. We believe that it is unlikely for the pair to rise further. After a minor bullish correction, the aussie is expected to fall towards the medium-term target of 0.6275.