S&P 500

Overview on July 1

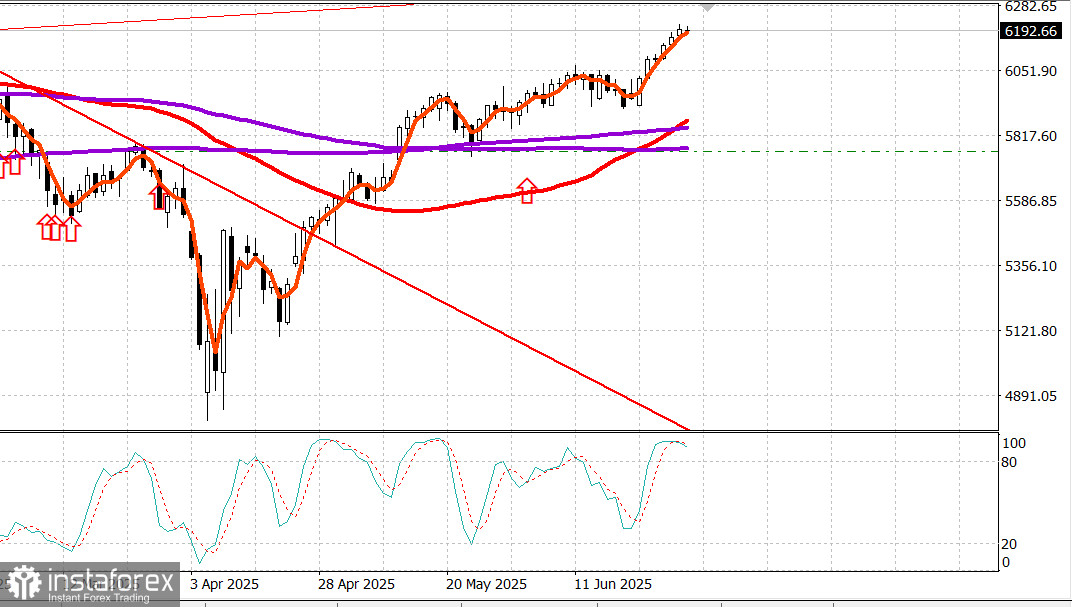

US market pauses at highs

Major US indices on Monday: Dow +0.6%, NASDAQ +0.5%, S&P 500 +0.5%, S&P 500: 6,204, trading range: 5,700–6,300.

The S&P 500 and Nasdaq Composite set record highs on Friday, and nothing prevented them from continuing their bullish move into record territory.

For a moment, it looked like there might be some obstacle in these moves, but a surge of buying interest in Apple (AAPL 205.17, +4.09, +2.03%) occurred in the second half of the day after a Bloomberg report said the company was considering using external AI assistance to power its new version of Siri.

Apple was just below $200 pet share when the news hit, but traded up to $207.39 afterward.

That was a sizable weight in market capitalization, which ultimately fueled the push above 6,200 for the S&P 500 on the last trading day of a remarkable second quarter, in which the S&P 500 gained 10.6% and the Nasdaq Composite jumped by 17.8%.

However, these gains don't even show half the full picture. Compared to the lows of April 7, the S&P 500 and Nasdaq Composite have climbed by 28% and 38%, respectively.

Before the Apple headlines, the session was filled with political news that was largely interpreted in a positive light.

The Senate held a procedural vote over the weekend that paved the way for a full Senate vote late Monday or early Tuesday on its version of the "One Big Beautiful Bill."

This bill, among other things, would extend the 2017 tax cuts for all income levels and make those cuts permanent. It introduces work requirements for Medicaid starting December 2026, phases out tax credits for solar and wind energy from December 2026, raises the SALT deduction cap to $40,000 for individuals earning $500,000 or less for a five-year period (after which it reverts to $10,000), and increases the debt ceiling by $5 trillion.

If the Senate passes the bill, which the CBO estimates would add $3.3 trillion to the deficit over the next decade, it will move to the House of Representatives for consideration and create the possibility of being sent to the president's desk for signing by July 4.

A comforting element for the stock market in all this was that the Treasury market did not revolt over the CBO's assessment. In fact, the Treasury market staged a modest rally, showing gains across the curve led by longer maturities.

The yield on the 2-year note fell by two basis points to 3.72%, while the yield on the 10-year note dropped by six basis points to 4.23%. Alongside developments around the "One Big Beautiful Bill," there were reports highlighting Canada's efforts to restart negotiations with the US by repealing the digital services tax, and speculation that other trade deals could be announced soon, including the possibility of reaching an agreement with the EU.

Separately, it was welcome news for capital markets to hear that all major banks passed the Federal Reserve's stress test. This news was released after Friday's close and opens the door for banks to announce capital return plans. Investment banks, led by Dow component Goldman Sachs (GS 707.75, +16.94, +2.45%), which hit its own record high, set the pace for gains in the financial sector (+0.9%).

The only other sector that outperformed financials today was information technology (+1.0%), which rallied around Apple and AI-related trading fueled by encouraging comments from Oracle (ORCL 218.63, +8.39, +3.99%) regarding its cloud business.

For the quarter, the information technology sector rose by 23.5%. Most sectors ended the day higher. The only two laggards were consumer discretionary (-0.9%) and energy (-0.7%).

S&P 500: +5.5%Nasdaq: +5.5%DJIA: +3.6%S&P 400: -0.6%Russell 2000: -2.5%

Data recap: Chicago PMI for June (actual 40.4; consensus 43.4; prior 40.5)

Energy: Brent crude at $66.80 — unchanged on the day

Conclusion: The S&P 500 crossed above the 6,200 level yesterday. However, the index has not consolidated there yet and is pulling back during Tuesday's session. We recommend holding long positions and awaiting key developments later in the week.