After markets spent Monday focused on the scandal surrounding L. Cook, the Fed's chief economist, and responded to the fading theme of trade wars, attention is now turning to the release of critical US labor market data—numbers that have the potential to fully reshape the conversation about the need for a Fed rate cut.

Let us start with Wednesday's JOLTS job openings report for July. The data revealed a significant decline versus both consensus (7.181 million versus 7.380 million forecast) and the previous number, which was revised downward to 7.357 million.

These figures clearly illustrate that in July, the US labor market started to slow across the board, a trend already signaled by previous releases from ADP and the Department of Labor. Now, markets are focused on today's ADP employment report for the private sector. According to consensus, the US economy was expected to add 73,000 private payroll jobs in July versus 104,000 the previous month. Should the actual data come in line with expectations, or lower—or even slightly higher, but below 100,000—it would be a strong confirmation of labor market cooling. Paradoxically, such negativity would be interpreted as good news. In that case, participants will act on the classic principle "bad news is good news," because it would open the door to a 0.25% Fed rate cut at the September 17 meeting.

While the ADP report is not comprehensive and does not capture the full spectrum of the US labor picture, it can still spark increased demand for equities in anticipation of Friday's official non-farm payrolls data from the Department of Labor.

How could markets react to weak US labor data?

As I have previously noted, the prospect of a Fed rate cut is now the central issue for markets. It is a pivotal question that can alter the broader outlook. A rate cut would lead to lower yields on deposits and bonds, providing a catalyst for dollar weakness in the Forex market. However, as mentioned earlier, any dollar decline will likely be limited since many of the other currencies in the dollar basket are also grappling with significant economic headwinds. This especially applies to Western economies such as the UK, the EU, Australia, and similar markets.

A weaker dollar may support gold prices, but the impact is likely to be marginal, as Fed easing has already been largely priced in and there are few expectations that reduced geopolitical risks, such as an easing Ukraine situation, will drive fresh demand for gold.

The cryptocurrency market, particularly those assets paired with the dollar, could see some limited short-term support following a rate cut. Still, the effect is unlikely to last long, as yield-generating assets, such as dividend-paying equities, remain more attractive in this scenario.

The assessment of the overall market environment is moderately positive.

Forecast for the day:

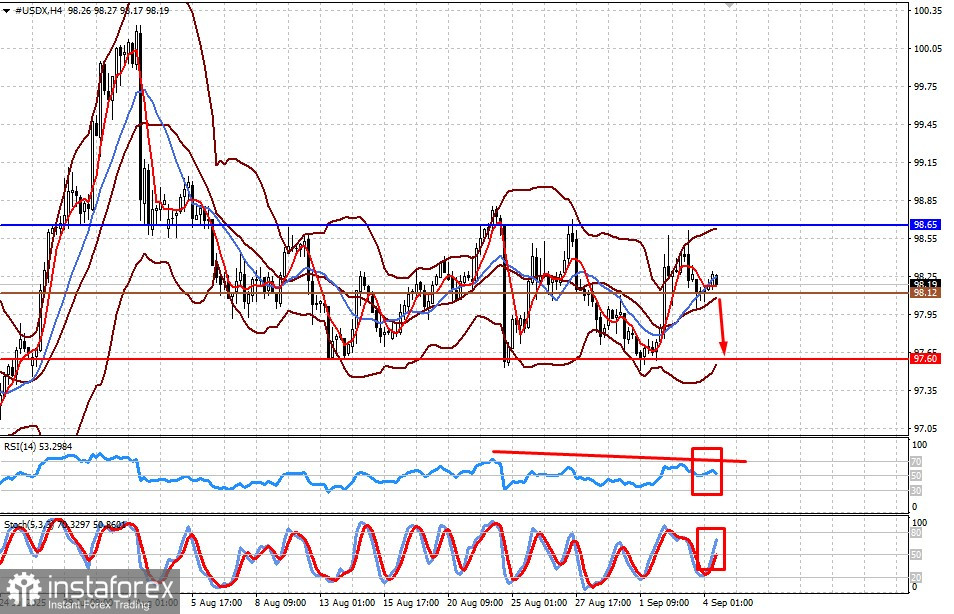

#USDX

The dollar index remains in a broad range of 97.60–98.65 in anticipation of the US jobs data. Should the ADP and Department of Labor reports come in below forecasts, the index could fall toward 97.60. The 98.12 mark may serve as a level for potential selling.

AUD/USD

The pair is still trading sideways but could pivot higher and target 0.6560 on the back of the ADP report. The 0.6527 level might be a good entry point for buying.