US equity indices closed sharply lower yesterday. The S&P 500 lost 0.55%, while the Nasdaq 100 dropped 0.95%. The Dow Jones Industrial Average gave back 0.15%.

Asian stocks advanced after Chinese technology shares surged. Alibaba Group Holding Ltd. pledged to boost investment in artificial intelligence, fueling gains. Chinese semiconductor stocks joined the rally after Morgan Stanley raised its outlook for the sector and Huawei Technologies Co. announced plans to overtake Nvidia Corp. in AI chip production. Alibaba shares climbed 7.8% in Hong Kong. The MSCI Asia Equity Index added just 0.1%.

Futures for European equity indices started the session on a weak note, while US contracts gained a modest 0.1%. Oil prices rose, supported by strong rhetoric from President Donald Trump against Russia. US Treasury yields remained elevated after Federal Reserve Chair Jerome Powell warned of persistent risks in the labor market and inflation, and noted that policymakers face a challenging path ahead as they consider further monetary easing. Gold traded near record highs.

Powell's statements acted as a catalyst for risk repricing, prompting investors to seek safety in government bonds and other defensive assets. In a complicated macro environment, where data points to slowing economic growth but inflation remains uncomfortably high, every remark from Powell is scrutinized. The labor market, in particular, remains a key indicator the Fed is closely monitoring—as a strong job market can fuel inflationary pressures, while softness could signal a looming recession.

This year, US equity indices have risen as fears of Trump's trade war ebbed and investors speculated on continued Fed rate cuts. However, at present, there are few new drivers for a continued bull market. The start of earnings season could provide new momentum, and that will soon be put to the test.

Oil continued to rally amid growing risks to Russian supplies, including Ukrainian strikes on energy infrastructure and worsening tensions with NATO. Brent crude climbed to $68 per barrel following a 1.6% increase on Tuesday. Russia is also considering export restrictions on diesel fuel for certain companies.

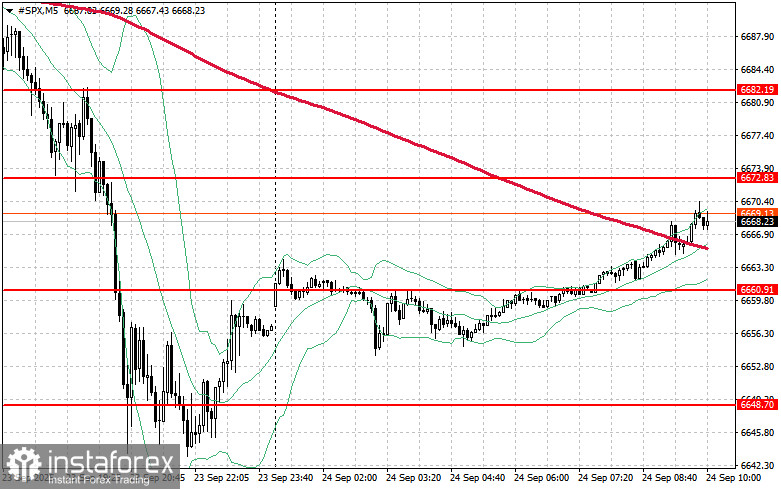

From a technical perspective, S&P 500 buyers today will need to clear the closest resistance at $6,672 to keep any recovery intact, with a breakout opening the way for a move to $6,682. Holding above $6,697 is equally important for strengthening the bulls' position. If risk appetite wanes and the index moves lower, buyers must show support around $6,660. A decisive loss of this area could quickly send the index down to $6,648 and further toward $6,624.