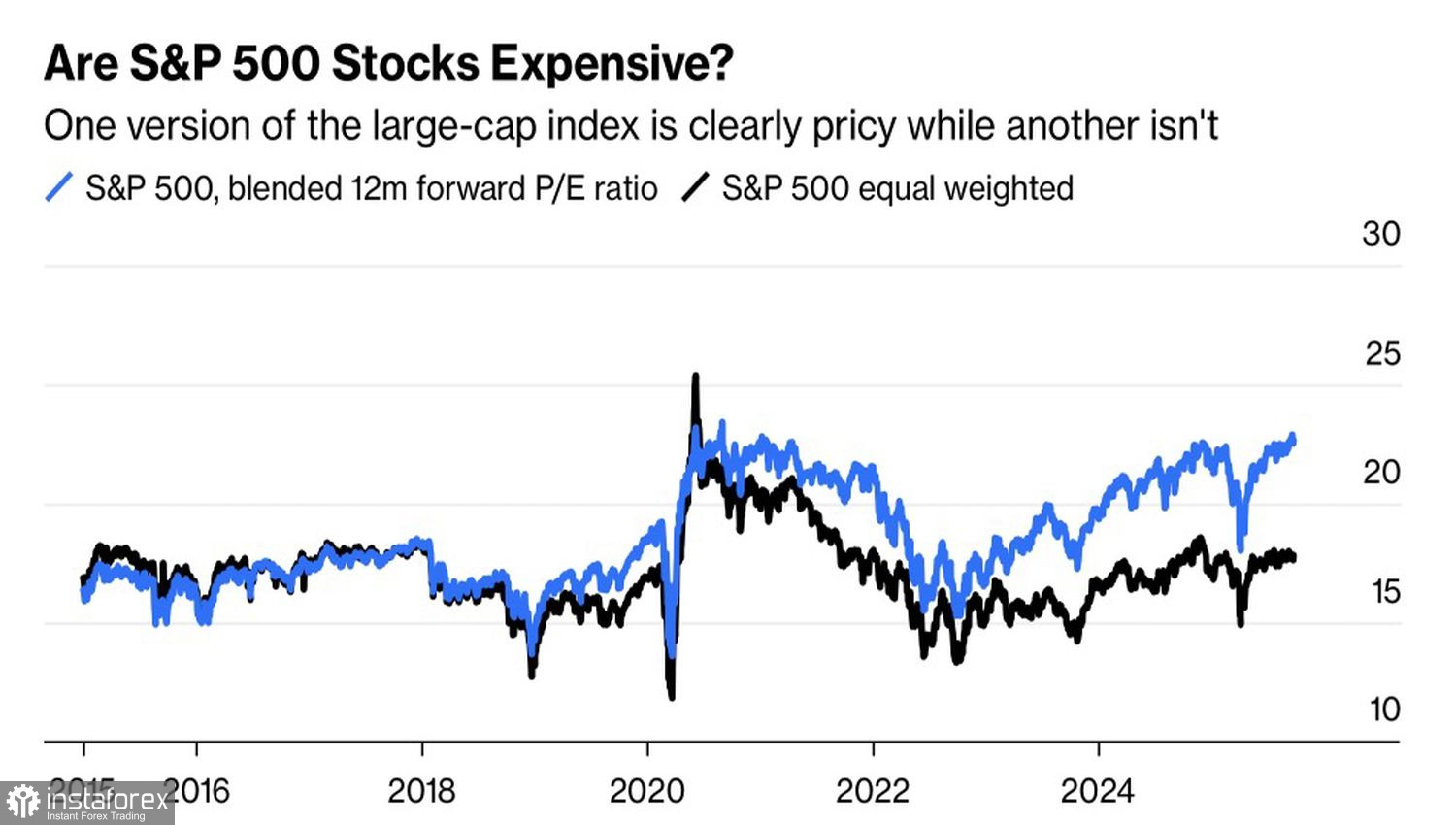

If new U.S. tariffs and the looming government shutdown haven't spooked markets, should investors really be worried about lofty valuations? The S&P 500 is currently trading at nearly 23 times the earnings expected over the next 12 months. Over the past 25 years, such levels have been seen only twice — during the dot-com bubble and the pandemic. Yet some individual companies are trading at even higher P/E multiples.

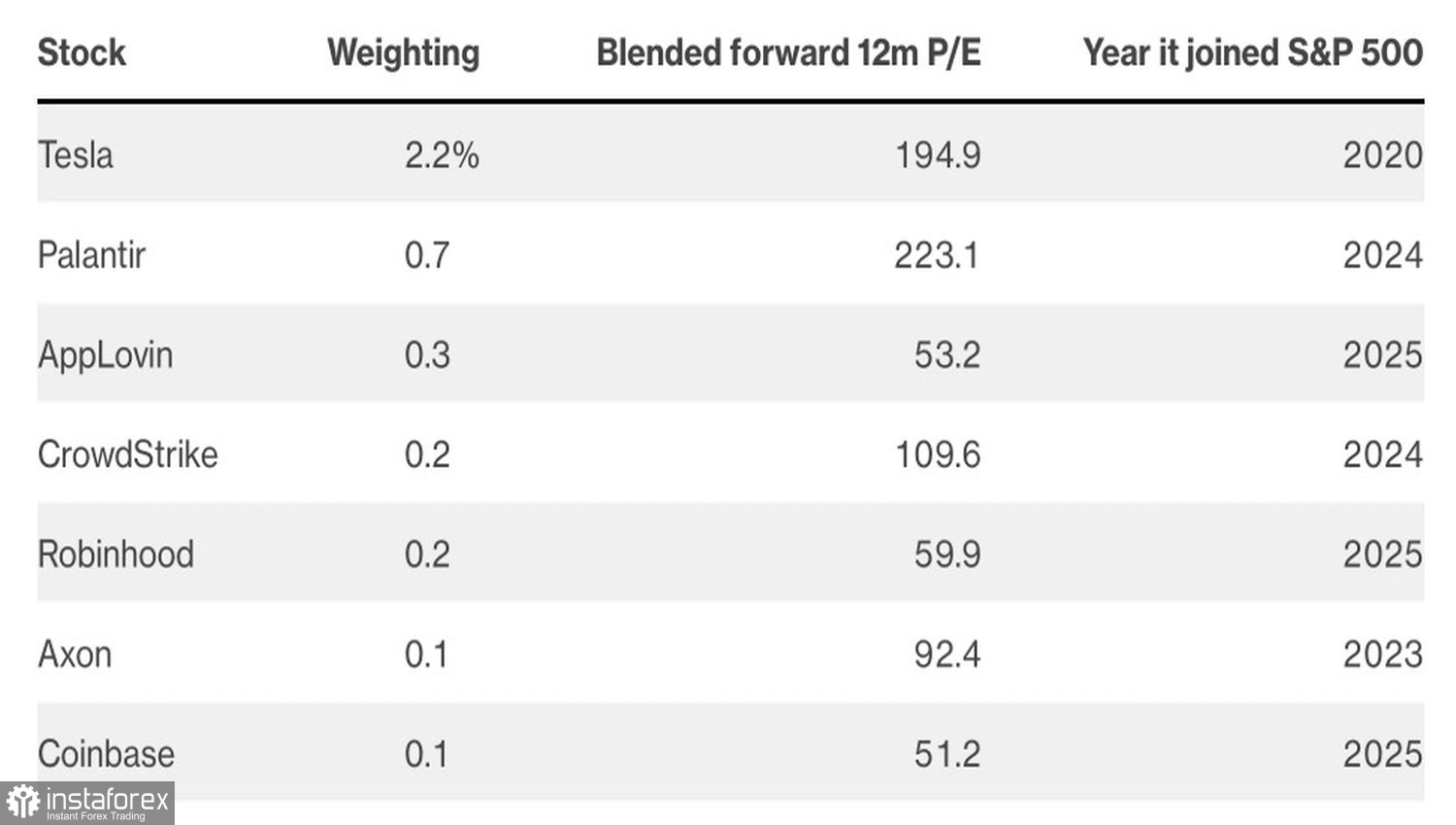

U.S. Companies With Elevated Valuations

Interestingly, it is precisely the stocks with inflated valuations that are leading the rally. On September 29, the S&P 500 gained on the back of a 12% surge in Robinhood, whose P/E stands at 60. Since the beginning of the year, Robinhood shares have tripled.

Some analysts argue that the environment has undergone significant changes. Whereas the average probability of a U.S. recession stood at 42% before World War II, it has dropped to just 10% over the past three decades. The U.S. has shifted from an industrial economy to one dominated by technology and services. The share of mega-cap companies in the S&P 500 has grown significantly. Indeed, if weighted averages rather than market capitalization were used, the P/E of the broad index would fall to 17.8 — close to its 10-year average.

S&P 500 Valuations in Perspective

As a result, valuation metrics are becoming less relevant for investment decisions compared to corporate earnings, macroeconomic conditions, and Federal Reserve policy. Moreover, the U.S. market holds one critical advantage over others — leadership in artificial intelligence technologies.

It is no surprise that, instead of fleeing after U.S. Independence Day, foreign investors have increased their exposure to American assets. In the three months ending June 30, they purchased $290 billion in equities. Foreign investors now hold around $18 trillion worth of U.S. stocks, equal to 30% of the $60 trillion market.

Thanks to strong foreign demand and a lack of fear over high valuations, the S&P 500 has already notched roughly 30 record highs this year and seems able to shrug off new White House tariffs and the risk of a government shutdown. Historically, disagreements between Republicans and Democrats have usually been resolved at the last minute. The market will only start to price in shutdown risks if the standoff drags on for several days.

Far more important for equities was the latest speech by New York Fed President John Williams, who described tariff-driven inflation as temporary and reaffirmed that the Fed's decision to cut rates was the right one.

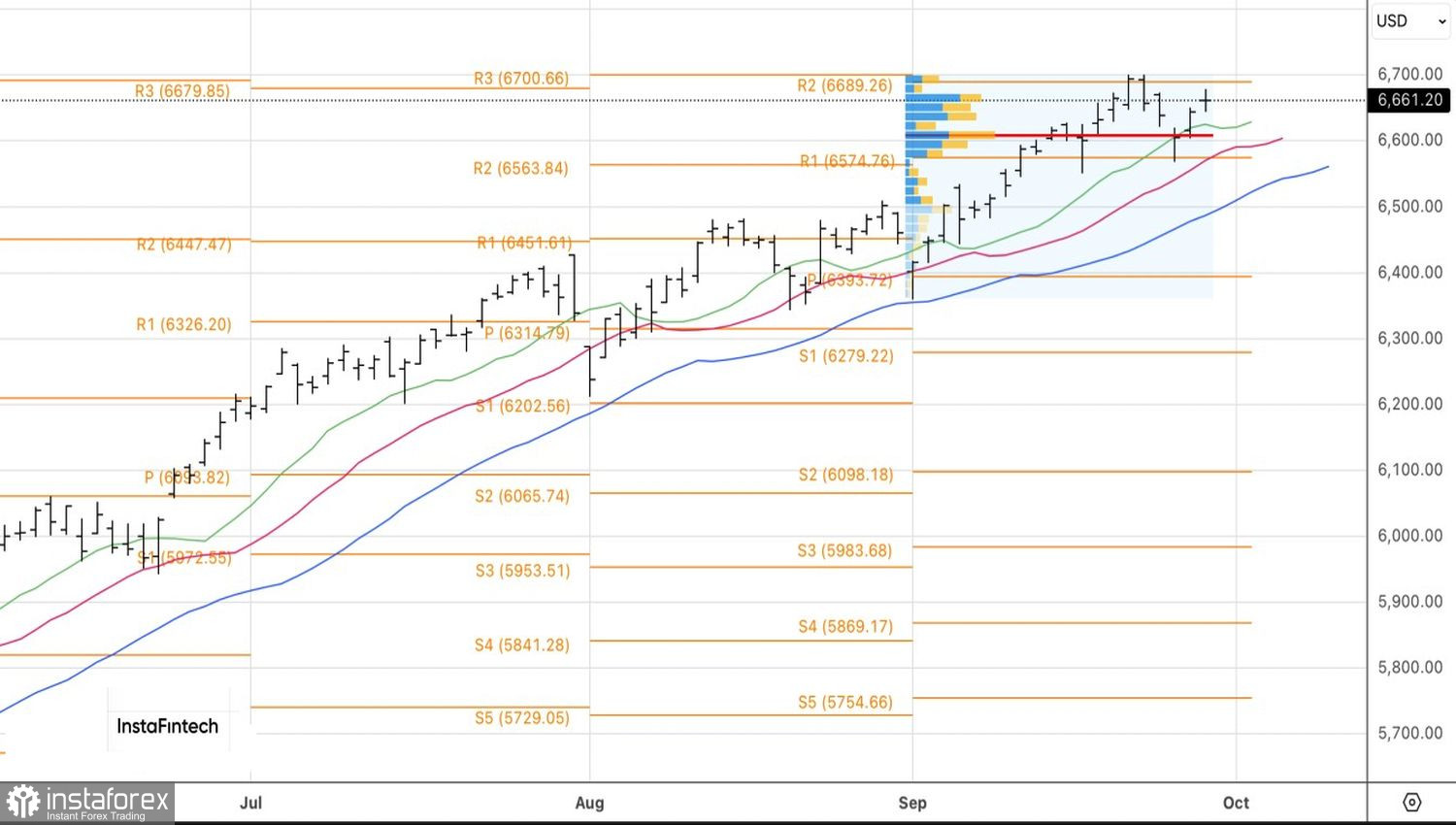

Technical Outlook

On the daily chart, the S&P 500 rally remains intact. Long positions opened at 6,570 and 6,610 should be held for now. However, the growing risk of reversal patterns such as 1-2-3 or a Double Top may prompt profit-taking. A necessary trigger would be a drop below the doji bar low at 6,640.