The storm in the U.S. equity market shows no signs of calming. The S&P 500 opened with a gap for the second consecutive trading session—this time to the downside—following news of an escalation in the trade conflict. Beijing effectively barred Chinese companies from doing business with the U.S. subsidiary of South Korean shipbuilding giant Hanwha Ocean. Yet upbeat corporate earnings and dovish comments from Jerome Powell helped the broad market index ride the volatility rollercoaster and rebound.

Financial results from major banks, including Goldman Sachs, JPMorgan Chase, and Wells Fargo, exceeded expectations, while BlackRock announced that assets under management surpassed $13 trillion for the first time in history. According to FactSet, third-quarter earnings for S&P 500 companies are expected to rise by 8%. The actual figures could come closer to 13%. Historically, earnings have beaten estimates in three out of every four quarters, which has been a strong support for the U.S. stock market.

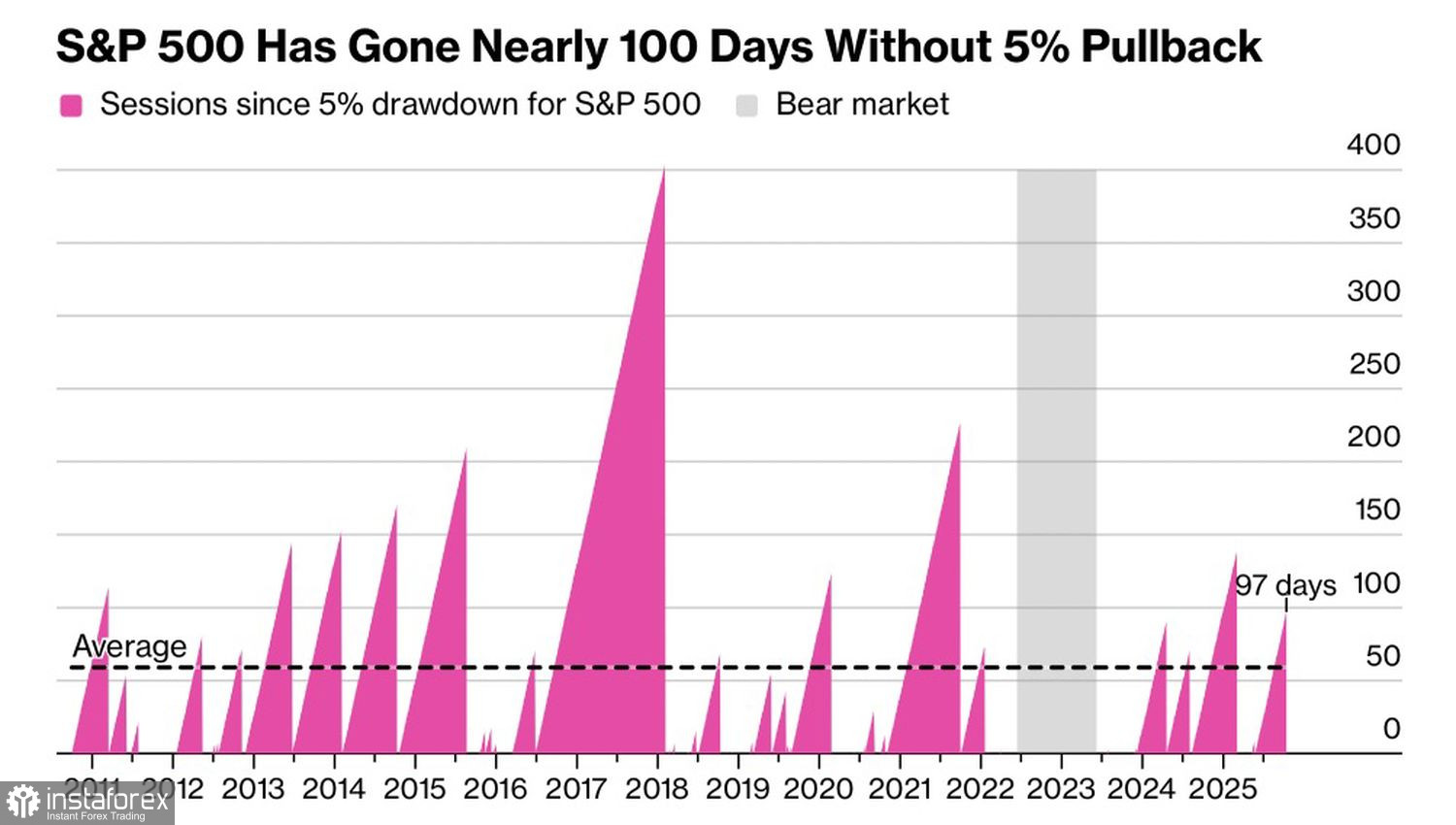

On the other hand, the S&P 500 bull market has now stretched into its fourth year, and the index hasn't experienced at least a 5% pullback in 97 trading sessions. The long-term average for such streaks is just 59 days. This raises the question: Is it time for a correction?

Chart: S&P 500 Streaks Without 5% Drawdowns

A return of trade war tensions could be the trigger. Beijing is playing hardball—it seems to have found Donald Trump's Achilles' heel: his unwillingness to see stock indices decline. The president views them as a personal success metric. After the market closed, he announced 100% tariffs, only to reassure the public on social media shortly afterward with posts like "Everything will be fine with China" and "The United States doesn't want to hurt China; we want to help!"

Markets react quickly to messages from the White House and continue to buy S&P 500 dips under the TACO strategy. But China may well believe that Trump will eventually yield. If not, the standoff could escalate into a full-blown trade war, triggering a meaningful correction in the S&P 500 and weighing down both the U.S. and global economies. The Fed would then be left with no choice but to cut rates aggressively.

Jerome Powell gave no concrete indication that another round of monetary easing would occur in October. However, he did note that a continued slowdown in job growth would eventually lead to higher unemployment. Despite another round of blows traded between Beijing and Washington, the S&P 500 managed to edge upward, though it retreated slightly as the trade tension news settled. China halted soybean purchases from the U.S., and in return, the U.S. will stop buying vegetable oil from Chinese exporters.

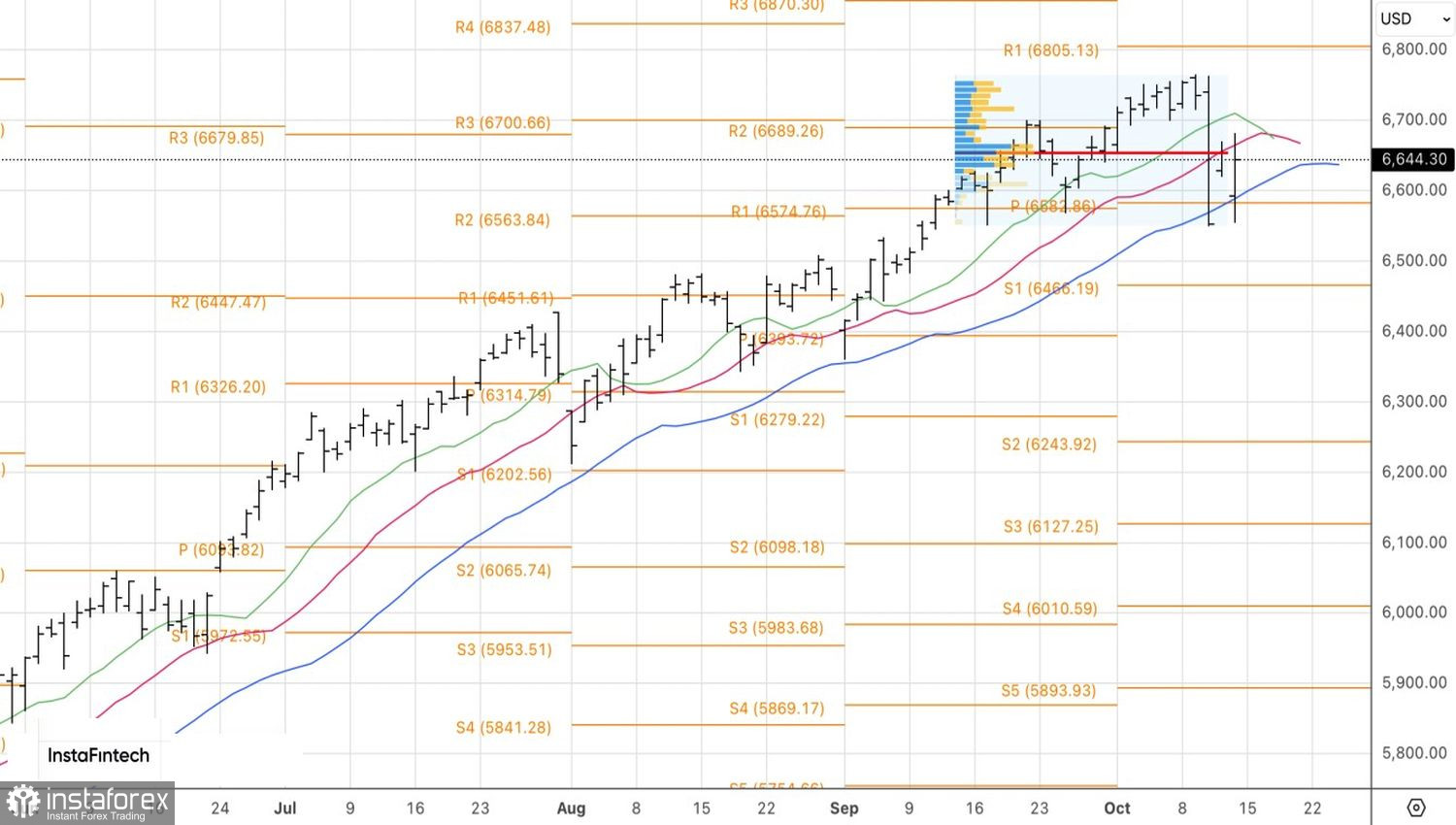

From a technical perspective, the S&P 500 on the daily chart has twice tested an inside bar pattern. Bulls have yet to close a session above fair value at the 6655 level. A breakout above the large-bar high at 6680 would be a buying signal. On the other hand, a failure to reclaim the 6655 resistance would increase the likelihood of a correction and raise the case for entering short positions.